Executive Summary

As the United States rapidly becomes both a more diverse and unequal nation, policymakers face the urgent challenge of confronting growing wealth gaps by race and ethnicity. To create a more equitable and secure future, we must shift away from public policies that fuel and exacerbate racial disparities in wealth. But which policies can truly begin to reduce our country’s expanding racial divergences?

Until now there has been no systematic analysis of the types of public policies that offer the most potential for reducing the racial wealth gap. This paper pioneers a new tool, the Racial Wealth AuditTM, and uses it to evaluate the impact of housing, education, and labor markets on the wealth gap between white, Black, and Latino households and assesses how far policies that equalize outcomes in these areas could go toward reducing the gap. Drawing on data from the nationally representative Survey of Income and Program Participation (SIPP) collected in 2011, the analysis tests how current racial disparities in wealth would be projected to change if key contributing factors to the racial wealth gap were equalized.

Main Findings

- The U.S. racial wealth gap is substantial and is driven by public policy decisions. According to our analysis of the SIPP data, in 2011 the median white household had $111,146 in wealth holdings, compared to just $7,113 for the median Black household and $8,348 for the median Latino household. From the continuing impact of redlining on American homeownership to the retreat from desegregation in public education, public policy has shaped these disparities, leaving them impossible to overcome without racially-aware policy change.

- Eliminating disparities in homeownership rates and returns would substantially reduce the racial wealth gap. While 73 percent of white households owned their own homes in 2011, only 47 percent of Latinos and 45 percent of Blacks were homeowners. In addition, Black and Latino homeowners saw less return in wealth on their investment in homeownership: for every $1 in wealth that accrues to median Black households as a result of homeownership, median white households accrue $1.34; meanwhile for every $1 in wealth that accrues to median Latino households as a result of homeownership, median white households accrue $1.54.

- If public policy successfully eliminated racial disparities in homeownership rates, so that Blacks and Latinos were as likely as white households to own their homes, median Black wealth would grow $32,113 and the wealth gap between Black and white households would shrink 31 percent. Median Latino wealth would grow $29,213 and the wealth gap with white households would shrink 28 percent.

- If public policy successfully equalized the return on homeownership, so that Blacks and Latinos saw the same financial gains as whites as a result of being homeowners, median Black wealth would grow $17,113 and the wealth gap between Black and white households would shrink 16 percent. Median Latino wealth would grow $41,652 and the wealth gap with white households would shrink 41 percent.

- Eliminating disparities in college graduation and the return on a college degree would have a modest direct impact on the racial wealth gap. In 2011, 34 percent of whites had completed four-year college degrees compared to just 20 percent of Blacks and 13 percent of Latinos. In addition, Black and Latino college graduates saw a lower return on their degrees than white graduates: for every $1 in wealth that accrues to median Black households associated with a college degree, median white households accrue $11.49. Meanwhile for every $1 in wealth that accrues to median Latino households associated with a college degree, median white households accrue $13.33.

- If public policy successfully eliminated racial disparities in college graduation rates, median Black wealth would grow $1,313 and the wealth gap between Black and white households would shrink 1 percent. Median Latino wealth would grow $3,528 and the wealth gap with white households would shrink 3 percent.

- If public policy successfully equalized the return to college graduation, median Black wealth would grow $10,786 and the wealth gap between Black and white households would shrink 10 percent. Median Latino wealth would grow $5,878 and the wealth gap with white households would shrink 6 percent.

- Eliminating disparities in income—and even more so, the wealth return on income—would substantially reduce the racial wealth gap. Yet in 2011, the median white household had an income of $50,400 a year compared to just $32,028 for Blacks and $36,840 for Latinos. Black and Latino households also see less of a return than white households on the income they earn: for every $1 in wealth that accrues to median Black households associated with a higher income, median white households accrue $4.06. Meanwhile, for every $1 in wealth that accrues to median Latino households associated with higher income, median white households accrue $5.37.

- If public policy successfully eliminated racial disparities in income, median Black wealth would grow $11,488 and the wealth gap between Black and white households would shrink 11 percent. Median Latino wealth would grow $8,765 and the wealth gap with white households would shrink 9 percent.

- If public policy successfully equalized the return to income, so that each additional dollar of income going to Black and Latino households was converted to wealth at the same rate as white households, median Black wealth would grow $44,963 and median Latino wealth would grow $51,552. This would shrink the wealth gap with white households by 43 and 50 percent respectively.

To effectively address the increasing inequality that is undermining Americans’ economic security, we must first identify the key factors contributing to the problem and evaluate policy proposals that could affect current trends. The Racial Wealth Audit is designed to fill the void in our understanding of the factors contributing to the racial wealth gap and clarify our ability to reduce the gap through policy. This paper, which presents the first analyses using this new tool, will be followed by a series of policy briefs using the Racial Wealth Audit to analyze specific public policies and policy proposals.

Introduction

America is becoming both a more diverse nation and a more unequal one. Over the past four decades, wealth inequality has skyrocketed, with nearly half of all wealth accumulation since 1986 going to the top 0.1 percent of households. Today the portion of wealth shared by the bottom 90 percent of Americans is shrinking, while the top 1 percent controls 42 percent of the nation’s wealth. At the same time, an increasing share of the American population is made up of people of color, and wealth is starkly divided along racial lines: the typical Black household now possesses just 6 percent of the wealth owned by the typical white household and the typical Latino household owns only 8 percent of the wealth held by the typical white household. These wealth disparities are rooted in historic injustices and carried forward by practices and policies that fail to reverse inequitable trends. As a result, racial wealth disparities, like wealth inequality overall, continue to grow.

Political thinkers increasingly recognize that rapidly growing inequality threatens economic stability and growth. But in a country where people of color will be a majority by mid-century, any successful push to reduce inequality must also address the structural racial inequities that hold back so many Americans. To create a more equitable future, we must confront the nation’s growing racial wealth gap and the public policies that continue to fuel and exacerbate it.

Stratospheric riches on the scale of the wealthiest Americans will never be accessible to the vast majority. Yet access to some degree of wealth is critical for every family’s economic security. Wealth functions as a financial safety net that enables families to deal with unexpected expenses and disruptions of income without accumulating large amounts of debt. At the same time, wealth can improve the prospects of the next generation through inheritances or gifts. Intergenerational transfers of wealth can play a pivotal role in helping to finance higher education, supply a down payment for a first home, or offer start-up capital for launching a new business. Because households of color have less wealth today, Black and Latino young adults are far less likely than young white people to receive a large sum—or any money at all—from family members to make these investments in their future. The result is that the racial wealth gap perpetuates from generation to generation, with profound implications for the economic security and mobility of future generations.

The racial wealth gap is reinforced by federal policies that largely operate to increase wealth for those who already possess significant assets. The Corporation for Enterprise Development finds that more than half of the $400 billion provided annually in federal asset-building subsidies—policies intended to promote homeownership, retirement savings, economic investment and access to college—flow to the wealthiest 5 percent of taxpaying households. Meanwhile, the bottom 60 percent of taxpayers receive only 4 percent of these benefits and the bottom 20 percent of taxpayers receive almost nothing. Black and Latino households are disproportionately among those receiving little or no benefit. Unless key policies are restructured, the racial wealth gap—and wealth inequality in general—will continue to grow.

In this paper, we assess the major factors contributing to the racial wealth gap, considering how public policies around housing, education, and labor markets impact the distribution of wealth by race and ethnicity. Each factor is evaluated using a new tool: the Racial Wealth Audit developed by the Institute on Assets and Social Policy (IASP) to assess the impact of public policy on the wealth gap between white and Black and Latino households with the aim of guiding policy development. The Racial Wealth Audit draws on a baseline of representative data discussed in this paper to provide an empirical foundation for existing wealth among groups and the major determinants of wealth accumulation. For more information on the primary data source–the Survey of Income and Program Participation (SIPP)—and the analysis techniques used in this study, please see the Appendix.

In this report, we briefly discuss the historic and policy roots of the wealth gap in each area and quantify the extent to which each policy area contributes to the current gap. Next, we look at the extent to which changes in housing, education, and labor market trends would affect the wealth gap—for example, the wealth impact of increasing the rate of Black and Latino homeownership to match white homeownership rates, and the impact of increasing the wealth returns that households of color receive as a result of homeownership to match white returns. We note policy ideas for reducing the racial wealth gap in each area.

The greatest utility of the Racial Wealth Audit is evident in this policy analysis. From the starting position of existing disparities, the Audit predicts wealth increases or decreases for affected populations according to the components of a proposed policy. The Audit uses the most conservative assumptions possible, avoiding overstating changes in the gap. Finally, the Audit provides insight into the impact of policies on the racial wealth gap within a discrete time period, such as 1 year or 5 years ahead.

The Racial Wealth Audit is designed to fill the void in our understanding of the racial wealth gap and enhance our ability to reduce the gap through policy. It is an essential new measurement framework for assessment to facilitate informed decisions about the role of policy in asset-building, economic stability, and the racial wealth gap. Equally important, it can prevent the unintended side effects of policies that are not explicitly aimed at household wealth or financial disparities, yet contribute to worsening inequality. For more on the Racial Wealth Audit see IASP’s 2014 paper, The Racial Wealth Audit: Measuring How Policies Shape the Racial Wealth Gap.

Defining the Racial Wealth Gap

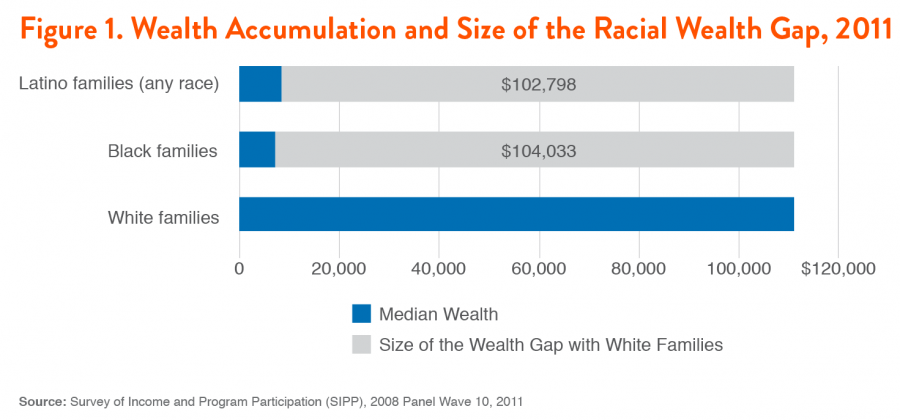

In this report, we define the racial wealth gap as the absolute difference in wealth holdings between the median household among populations grouped by race or ethnicity. In the U.S. the racial wealth gap shows that the typical white household holds multiple times the wealth of Black and Latino households. Using the SIPP, we estimate that the median white household had $111,146 in wealth holdings in 2011, compared to $7,113 for the median Black household and $8,348 for the median Latino household.

In relative terms, Black households hold only 6 percent of the wealth owned by white households, which amounts to a total wealth gap of $104,033, and Latino households hold only 8 percent of the wealth owned by white households, a wealth gap of $102,798 (see Figure 1). In other words, a typical white family owns $15.63 for every $1 owned by a typical Black family, and $13.33 for every $1 owned by a typical Latino family.

Terminology

This report analyzes data on white, Black, and Latino households. The terms Black and white are used to refer to the representative respondents of a household who identified as non-Latino Black or white in the Survey of Income and Program Participation (SIPP). Latinos include everyone who identified as Hispanic or Latino and may be of any race.

Throughout this report, we use the term “racial wealth gap” to refer to the absolute differences in wealth (assets minus debt) between Black and white households as well as between Latino and white households. All dollar figures are in 2011 dollars.

How Homeownership Contributes to the Racial Wealth Gap

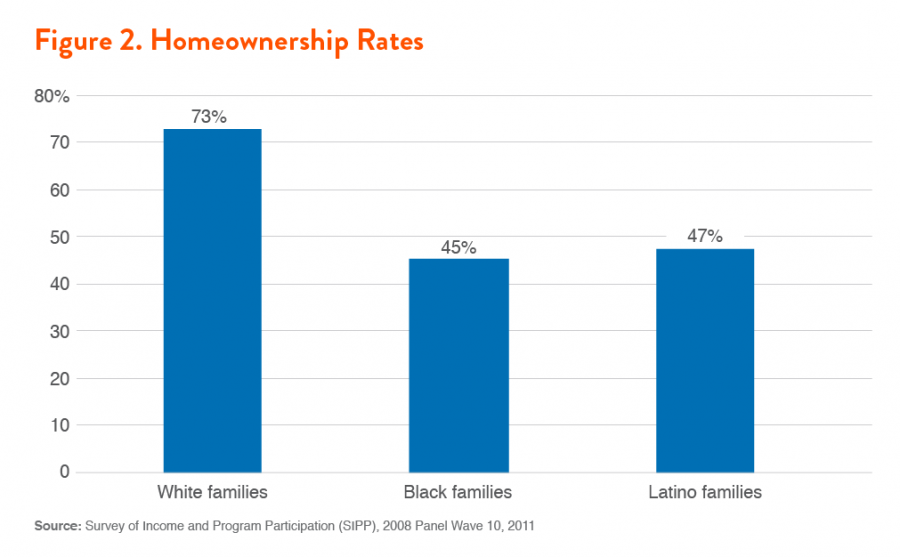

For most families in the U.S., home equity marks the largest segment in their wealth portfolio; however, home ownership is unequally distributed by racial and ethnic lines. Disparities in homeownership rates (73 percent of whites as compared to 47 percent of Latinos and 45 percent of Blacks [see Figure 2]), typical home equity ($86,800 for white homeowners at the median as compared to $50,000 for Black homeowners and $48,000 for Latino homeowners), and neighborhood values where whites and people of color live substantially contribute to the racial wealth gap. In addition, tracing the same households over 25 years revealed that the number of years a household owned their home explained 27 percent of the growing racial wealth gap. Because white families are more likely to receive inheritances and other family assistance to put a down payment on a home, they are often able to start acquiring home equity many years earlier than Black and Latino families, offering a valuable head start on wealth-building.

This section will explore the factors contributing to homeownership disparities in greater depth, and will analyze how equalizing rates of homeownership and returns to homeownership between whites, Blacks, and Latinos would each impact the racial wealth gap. We note that because the disparity in rates and returns to homeownership operate simultaneously to impair wealth building among households of color, policies that only address one aspect will not solve the entire portion of the racial wealth gap driven by homeownership.

Homeownership Policy Shapes the Wealth Gap

Lower homeownership rates among Blacks and Latinos have many roots, ranging from lasting legacies of past policies to disparate access to real estate ownership. The National Housing Act of 1934, for example, redlined entire Black neighborhoods, marking them as bad credit risks and effectively discouraging lending in these areas, even as Black home buyers continued to be excluded from white neighborhoods. While redlining was officially outlawed by the Fair Housing Act of 1968, its impact in the form of residential segregation patterns persists with households of color more likely to live in neighborhoods characterized by higher poverty rates, lower home values, and a declining infrastructure compared to neighborhoods inhabited predominantly by white residents.

Discriminatory lending practices persist to this day. When households of color access mortgages, they are more often underwritten by higher interest rates. Mainstream lending institutions were deeply implicated in discriminatory lending: in 2012 Wells Fargo Bank admitted that they steered thousands of Black and Latino borrowers into subprime mortgages when non-Hispanic white borrowers with similar credit profiles received prime loans. In addition, the proliferation of high-cost credit options such as payday lenders in many neighborhoods of color, combined with the scarcity of banks and credit unions, is another likely contributor to weak credit. The fact that Black and Latino families are more likely to have taken on subprime mortgages in recent years contributed significantly to the devastating impact of the housing collapse that began in 2006.

In addition to these longstanding homeownership and home equity disparities, the foreclosure crisis during the Great Recession of 2007-2008 dipped even further into families of color’s housing wealth. While the median white family lost 16 percent of their wealth in the housing crash and Great Recession, Black families lost 53 percent and Latino families lost 66 percent. Foreclosures both directly destroy housing wealth and have a lasting negative impact on credit, ensuring that mortgages and other loans will be offered on more costly terms in the future.

While homeownership plays a central part in building family wealth in the United States, the nation’s public policies have systematically operated to shut Black and Latino families out of numerous opportunities to build housing wealth that benefitted white families. Today, Latinos and Blacks are less likely to own their homes and accrue less wealth, at the median, as a result of homeownership than white families. The next two sections use empirical estimates to explore impacts on the racial wealth gap if these disparities were eliminated.

How Equalizing Homeownership Rates Affects the Wealth Gap

We tested the effects of equalizing homeownership rates among white, Black, and Latino families on the racial wealth gap. Our model looks at wealth accumulation by race and ethnicity if the existing home owning population among Black and Latino households matched the 73 percent rate of white families. In other words, what if Black and Latino homeowners made up 73 percent of each of their respective population subgroups, without changing typical home values for whites or households of color? The model did not control for other characteristics that might distinguish homeowners from non-homeowners.

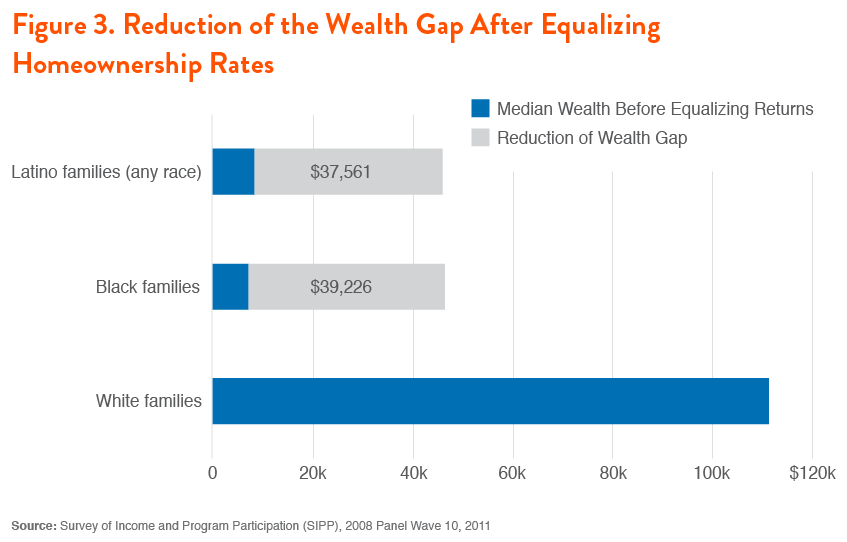

The results suggest that equalizing homeownership rates has substantial effects on the wealth accumulation of Black and Latino households. Median wealth among Black households rose from $7,113 to $39,226—adding $32,113 to the median Black household’s wealth (see Figure 3). Median wealth among Latino households rose from $8,348 to $37,561—adding $29,213 to the median Latino household’s wealth. Those numbers represent a 451 percent wealth increase for Black households, and a 350 percent wealth gain for Latino households.

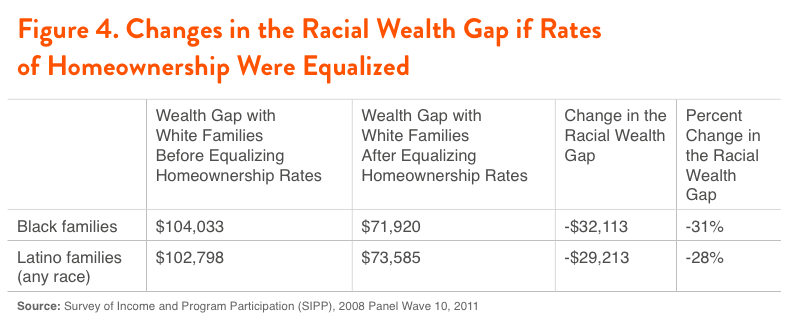

Equalizing Black and Latino homeownership rates with those of whites raises wealth among Black and Latino families, and substantially reduces the racial wealth gap. The wealth gap between white and Black families decreases by $32,113 to $71,920. This is a 31 percent reduction in the Black-white wealth gap. The wealth gap between white and Latino families decreases by $29,213 to $73,585, or a reduction of 28 percent (see Figure 4).

How Equalizing the Return to Homeownership Affects the Wealth Gap

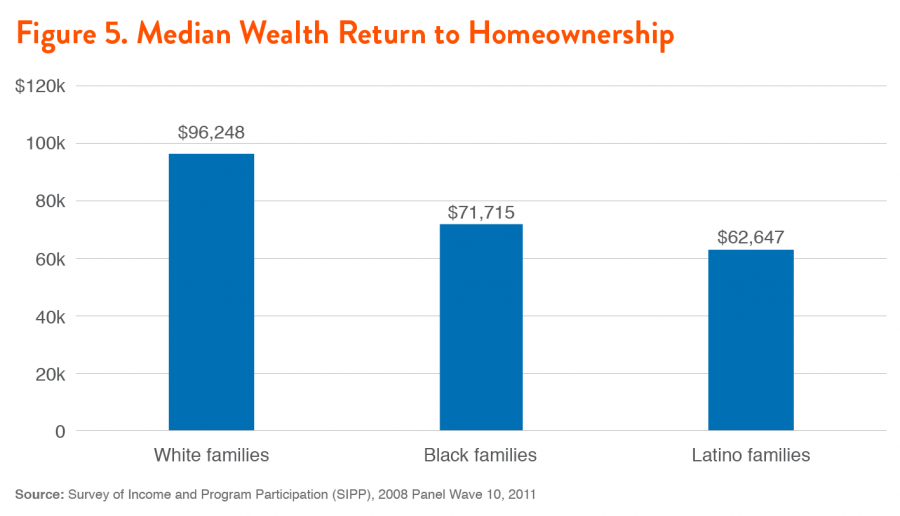

We tested the effects on the racial wealth gap of changing the wealth return on homeownership to Black and Latino households to equalize the return to homeownership for white households. The first step in this model estimates the wealth returns to homeownership using a multivariate median regression model for the white population. That model estimates that white households benefit from a $96,248 return on with homeownership.

Using a similar model to estimate the wealth effects of homeownership on Black households, we find that the wealth returns to homeownership for Black households amount to $71,715—just 75 percent of the returns that accrue to white households (see Figure 5). This difference of $24,533 means that for every $1 in wealth that a Black family builds as a result of homeownership, white families accrue $1.34. Meanwhile, the wealth returns to homeownership for Latino households amount to $62,647—just 65 percent of the returns that accrue to white households. This difference of $33,601 means that for every $1 in wealth that accrues to Latino families as a result of homeownership, white families accrue $1.54.

In order to construct a model that equalizes the returns to homeownership across groups, we assigned home equity at the rate accumulating to the median white household—$96,248—to Black and Latino households with home equity values less than that threshold. This assignment raises Black and Latino wealth by the difference between their existing median equity and the white median.

As a result of equalizing the return to Black homeownership to the level of return that accrues to whites, Black families’ median wealth grew by $17,113 to $24,226—a 241 percent increase in median Black household wealth (see Figure 6). As a result of equalizing the return to homeownership among Latinos to the level of return that accrues to whites, Latino families’ median wealth grew by $41,652 to $50,000—a 499 percent increase in Latino median wealth.

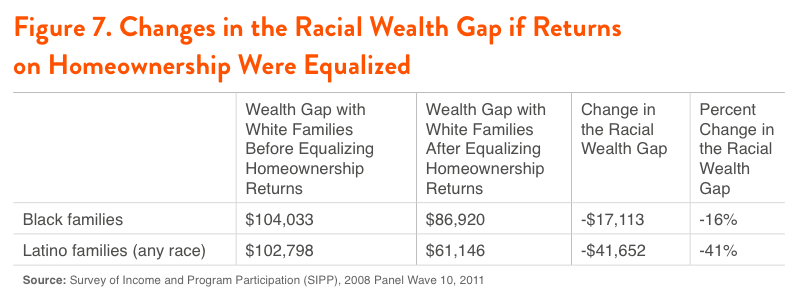

Equalizing wealth returns to homeownership raised wealth among Black and Latino families while white wealth was held constant, significantly reducing the racial wealth gap. Equalizing the returns to homeownership reduces the wealth gap between white and Black families by $17,133 to $86,920. This is a 16 percent reduction in the Black-white wealth gap (see Figure 7). Meanwhile the wealth gap between white and Latino families decreases by $41,652 to $61,146—a reduction of 41 percent.

Homeownership Policies to Reduce the Wealth Gap

Positing Black and Latino homeownership rates and returns equal to those of white families helps to clarify the contours of the racial wealth gap, but it’s quite different from having policy proposals that would actually accomplish these aims—or even approach them. Yet just as past and continuing policies have helped to shape the distribution of wealth in America today, policy change could alter the existing trends for better or worse. A bold, comprehensive approach would be required to move us towards the level of equality in homeownership modeled in our analyses; however, a number of policy efforts could bring us closer to expanding opportunities to build wealth through homeownership in the U.S. While far from a comprehensive list, here are three sample homeownership policies that could help to build housing wealth for people of color and shrink the racial wealth gap.

- Stricter enforcement of housing anti-discrimination laws. As noted above, residential segregation is a key reason that Black and Latino homeowners do not benefit from as great a rate of return on homeownership as their white counterparts. By limiting the residential market, segregation means that homes in predominantly Black and Latino neighborhoods accrue less value. Studies find that Black and Latino homebuyers still face barriers to purchasing homes in predominantly white areas. Stricter enforcement of housing anti-discrimination laws would increase the ability of people of color to buy homes in higher-value neighborhoods, offering significant potential for reducing the racial wealth gap.

- Authorizing Fannie Mae and Freddie Mac to reduce mortgage principal and make other loan modifications for struggling homeowners. As we’ve seen, Black and Latino homeowners are more likely than white homeowners to have obtained subprime mortgages and to have homes at risk of foreclosure. A policy that enables these federally-chartered institutions to reduce mortgage principal and modify mortgage loans in other ways that make them more sustainable would help to protect the home equity wealth of Black and Latino homeowners, potentially reducing the racial wealth gap.

- Lowering the cap on the mortgage interest tax deduction. As we have seen, typical Black and Latino homeowners own homes of less value than typical white homeowners. As a result, Black and Latino households benefit less from the tax deduction, which allow homeowners to deduct the cost of interest paid on up to $1 million in mortgage debt. A variety of different caps have been recommended, including an Obama Administration proposal to cap deductions at 28 percent for high-income households, those earning more than $250,000. Such a policy could be helpful in reducing the racial wealth gap, particularly if the additional tax revenues were used to fund foreclosure prevention programs and first-time homebuyers’ assistance programs, which are more likely to benefit Black and Latino households.

How Education Contributes to the Racial Wealth Gap

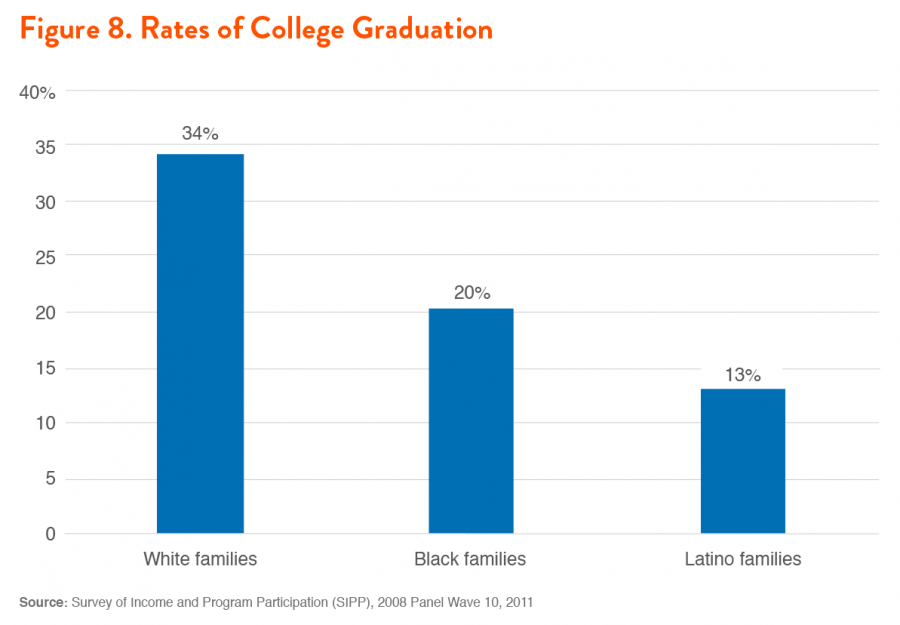

Attaining a college education has never been more important to a household’s ability to thrive in the labor market, attain financial stability, and build wealth. Today, more students than ever before are entering 4-year colleges. However, despite rising college attendance rates among Black and Latino households, barriers to completing a degree have actually widened the college attainment gap between whites and people of color over the past decade. In 2011, 34 percent of whites completed a four-year college degree, compared to just 20 percent of Blacks and 13 percent of Latinos (see Figure 8). One key barrier is the rapid growth in college costs, which forces households to take on significant debt in order to attend institutions of higher education—even in cases where students do not ultimately graduate. Gaps in college attainment by race and ethnicity also reflect other inequities in the K-12 education system and in household income.

In addition to attainment gaps, the returns to college education differ across racial and ethnic groups. At the median, a white family sees a return of $55,869 in wealth from completing a four-year college degree, while the median Black and Latino families attain just a small fraction of this return: $4,846 and $4,191 respectively. The returns to Black and Latino families are impacted by, among other things, their greater need to take on debt to pay for college and their disparate experiences in the labor market after graduation. According to previous research from IASP, differences in college completion rates accounted for about 5 percent of the growth in the racial wealth gap over a 25 year period (1984-2011).

This section looks more closely at the factors contributing to disparities in higher education, and evaluates how equalizing rates of college completion (defined as graduating with a four-year degree) and returns to college completion between whites, Blacks, and Latinos would each impact the racial wealth gap.

Education Policy Shapes the Wealth Gap

Public policy decisions are critical to understanding why Latinos and Blacks are less likely to have completed a four-year college degree than whites, as well as why Latino and Black graduates build less wealth as a result of their degrees. Educational inequities have deep historical roots in policies that prohibited slaves from learning to read and the century of substandard “separate but equal” educational facilities that followed, leaving many students of color poorly prepared for college. These past educational inequities matter today because parents’ educational level—as well as family incomes and wealth itself—significantly predict children’s educational success across their lifetimes. At the same time, contemporary policy choices, from the retreat from integration in K-12 education to the declining public support for affordable higher education, shape the educational opportunities available to youth of color who are more likely to need financial support for college, thereby contributing to the existing racial wealth gap.

Disparities in education begin early in the lives of children in the U.S. and current education policies often foster inequities. The policy decision not to invest in quality preschool education for all young people sets the stage for racial disparities that persist throughout the educational system from K-12 to higher education. While quality K-12 education is essential for college readiness, residential segregation leaves many Black and Latino students, particularly those from low-income families, concentrated in low-quality, under-resourced schools. As policy has shifted away from efforts to integrate public education that prevailed after the Brown v. Board of Education Supreme Court decision in 1954, research has documented dramatic increases in segregation, with Black and Latino students increasingly attending the same schools. Predominantly Black and Latino schools spend less per student than predominantly white schools, a disparity that is only partly accounted for by the different property-tax bases of school districts creating a highly unequal educational system across the country.

Once students reach college, racial and ethnic disparities in family economic resources and the soaring costs of attending college mean that students of color often confront unsustainable expenses as they pursue higher education, leading to huge debt burdens and lower graduation rates. At public institutions, increasing tuition and fees are primarily a result of declining state support for higher education shifting a greater share of the costs to students. As a result, Black and Latino students, with less family wealth than white students are more likely to struggle with higher costs, seek out less expensive schools, work excessive hours, reduce study time to work, and/or take on more student loan debt.

For young people who come from families without substantial wealth, education has long been seen as the pathway to greater opportunity and economic security. However rather than facilitating economic mobility, according to our analyses, current educational inequalities end up being a small, direct net contributor to the racial wealth gap. In addition, it is also likely influencing a number of other variables that shape unequal asset-building opportunities. The next two sections present our empirical analysis exploring how the racial wealth gap would change if educational disparities were reduced.

How Equalizing College Graduation Rates Affects the Wealth Gap

We tested the effects of equalizing college graduation rates among white, Black, and Latino families on the racial wealth gap. This test did not control for other characteristics that might distinguish those who finish college from those who do not. Instead, it looks at wealth accumulation by race and ethnicity if the proportion of Black and Latino households with a college degree matched the 34 percent college completion rate of whites.

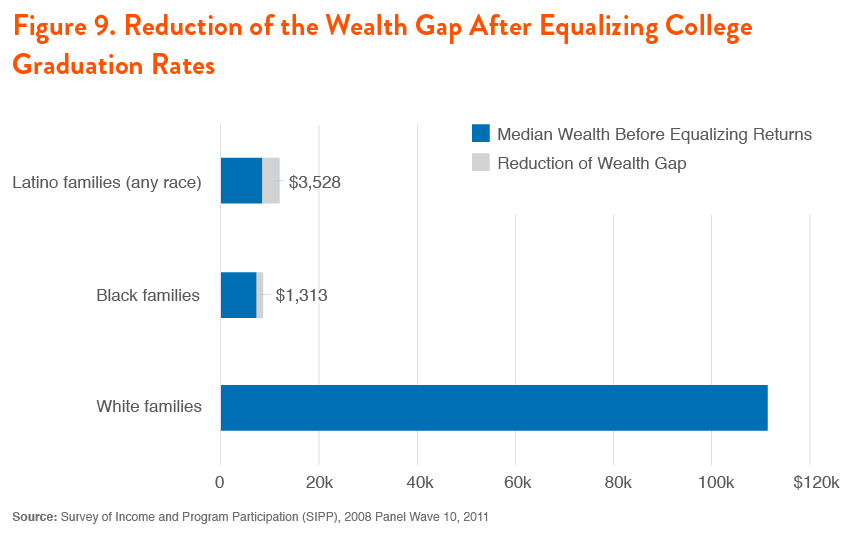

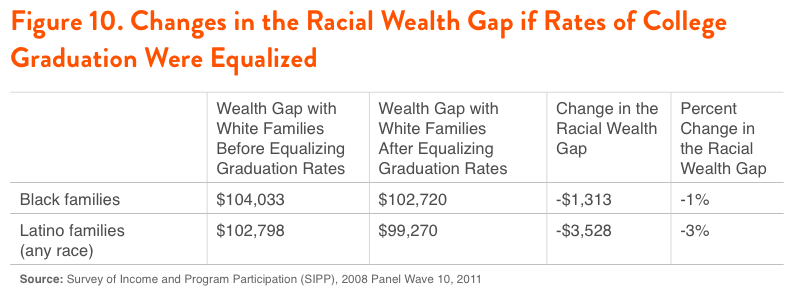

Compared to the effects of changes in homeownership rates on the racial wealth gap, the effects of changing college attainment rates on household wealth for Black and Latino families are modest. Median wealth among Black households rises from $7,113 to $8,426—adding $1,313 to the median Black household’s wealth (see Figure 9). Median wealth among Latino households rises from $8,348 to $11,876—adding $3,528 to the median Latino household’s wealth. Those gains represent an 18 percent wealth increase for Black households, and a 42 percent wealth increase for Latino households.

The equalization of college graduation rates raised wealth among Black and Latino families while white wealth was held constant, modestly reducing the racial wealth gap. The wealth gap between white and Black families was reduced by $1,313, which amounts to just 1 percent of the racial wealth gap (see Figure 10). The wealth gap between white and Latino families was reduced by $3,528, a reduction of 3 percent.

The fact that the reduction in the racial wealth gap from equalizing college graduation rates is small does not automatically imply that raising educational attainment is an ineffective means of closing the racial wealth gap. Instead, it suggests that matching the current levels of college degree attainment of white households—in which the benefits of a four-year college degree reach only about a third of households—is unlikely to substantially reduce the wealth gap.

How Equalizing the Return to College Graduation Affects the Wealth Gap

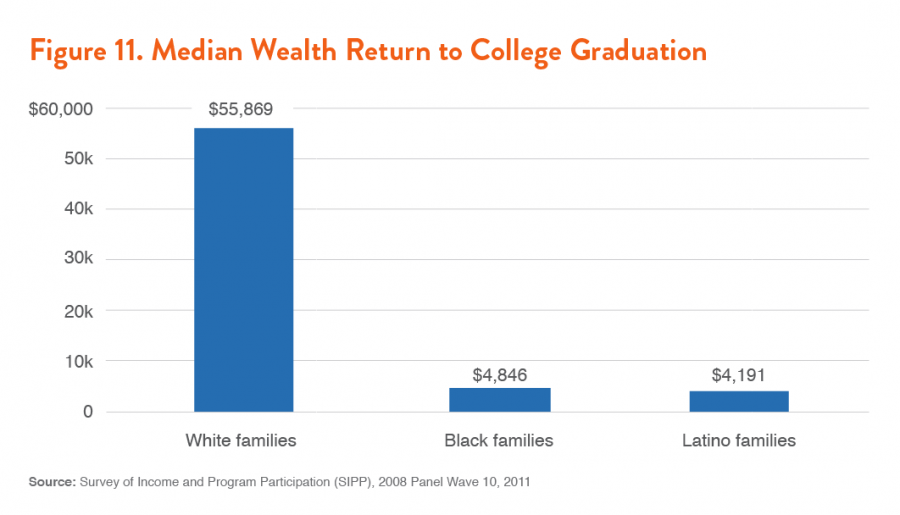

Next, we tested the effects on the racial wealth gap of changing the return on completing a four-year college degree for Black and Latino households to equal the return to graduation of white households. As seen above, the first step in this process estimates the wealth returns to a college degree using a multivariate median regression model for the white population. That model estimates that white households benefit from a wealth return of $55,869 associated with college graduation.

In analyzing the experiences of Black households, the wealth returns to a college education for Black households amount to just $4,846—only 9 percent of the returns that accrue to white households (see Figure 11). This difference of $51,023 means that for every $1 in wealth that accrues to Black families associated with a college degree at the median, white families accrue $11.49. Meanwhile, the wealth returns to a college education for Latino households amount to $4,191—just 8 percent of what accrues to white households. This difference of $51,678 means that for every $1 in wealth that accrues to Latino families from a college education, white families accrue $13.33.

In order to construct a model equalizing the returns to a college education across groups, we assigned Black and Latino households that had completed college with a value of total wealth equal to the return to college graduation for the median white household: $55,869. Black and Latino college graduates who already had household wealth above this value did not have their wealth adjusted. This change does not alter the differential rates of college graduation and thus affects only a subset of the Black and Latino populations.

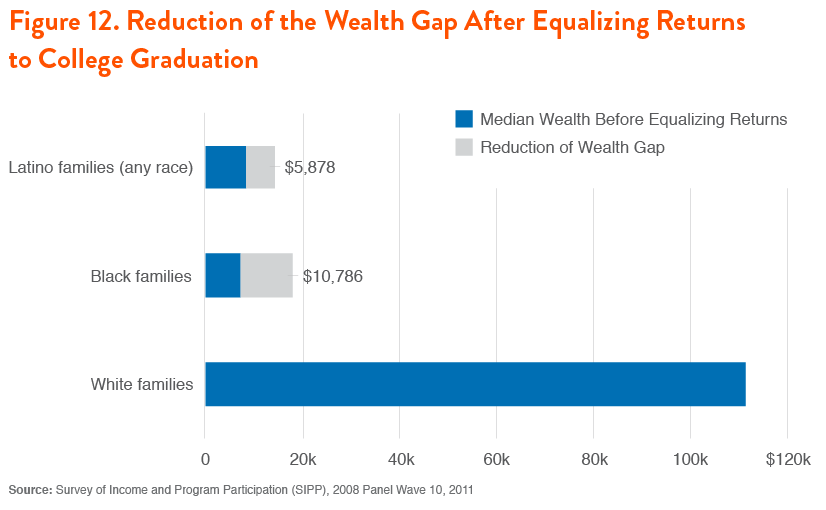

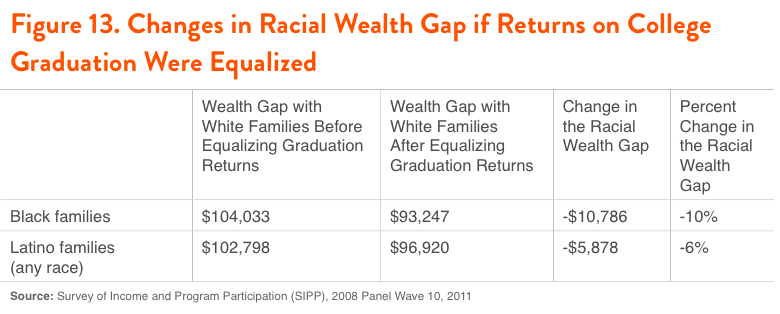

As a result of equalizing the return to a college education to the level of return accruing to whites, Black families’ median wealth grows by $10,786 to $17,899—a 152 percent increase in Black household wealth (see Figure 12). As a result of equalizing the return to a college education to the level of return accruing to whites, Latino families’ median wealth grows by $5,878 to $14,226—a 70 percent increase in Latino wealth.

The equalization of returns to a college education raises the medial level of wealth among Black and Latino families, while white median wealth remains constant, modestly reducing the racial wealth gap. Equalizing the returns to a college education reduces the wealth gap between white and Black families by $10,786 to $93,247. This is a 10 percent reduction in the Black-white wealth gap (see Figure 13). Meanwhile, the wealth gap between white and Latino families decreases by $5,878 to $96,920—a reduction of 6 percent.

One reason the reduction in the racial wealth gap is modest when the return to college education is equalized is because the affected households—the 20 percent of Blacks and 13 percent of Latinos that have attained a four-year college degree—is a relatively small proportion of the overall Black and Latino population. Raising college completion rates at the same time that the returns to a college degree increase would be expected to impact a greater number of households and to decrease the racial wealth gap more significantly.

Education Policies to Reduce the Wealth Gap

Disparities in attaining a college education account for only a small portion of the racial wealth gap. Our findings suggest that increasing college completion rates among Black and Latino youth and improving their returns on a college degree would reduce the wealth gap only modestly at the median. Nevertheless, a number of promising education policies do show potential to make a difference in shrinking racial wealth disparities. The following sample policies are not a comprehensive list:

- Invest in universal, high-quality preschool education. Black and Latino children see some of the greatest benefits from attending preschool, but many three- and four-year-olds lack access to affordable early childhood education. Establishing universally-available public preschool as a growing number of cities are now doing has the potential to reduce the racial wealth gap by helping students of color to enter school better-prepared to learn.

- Make K-12 education funding more equitable. Black and Latino students are more likely to attend under-resourced schools with less experienced teachers and fewer advanced courses, leaving them less well-prepared for college than their white counterparts. Federal, state, and district funding systems could be improved to address disparities. At the federal level, Black and Latino students would benefit from school funding formulas under Title I of the Elementary and Secondary Education Act that better target funding to schools with high concentrations of students in poverty. At the state level, funding systems that draw primarily on local property taxes could be re-envisioned, as they reflect residential segregation patterns along racial lines. Local governments also need to reconsider racialized patterns of funding distribution within school districts.

- Recommit to racially integrated schools, colleges, and universities. While recent Supreme Court decisions have made it difficult to promote the racial and ethnic integration of public schools, there is substantial evidence that de-segregation worked to reduce racial disparities and produce a sense of common educational fate among students of different racial and ethnic groups. Therefore, policies that promote racially and ethnically integrated schools have the potential to decrease racial and ethnic wealth disparities.

- Establish an Affordable College Compact. Greater state investment in public higher education would help to ensure that Black and Latino students can attend college without incurring debt or experiencing financial hardship. Lower college costs would enable more students of color to enroll in and complete college. At the same time, eliminating the need to take on debt would increase the return to a college degree. The federal government could encourage states to reinvest in higher education by offering higher education matching grants to states that commit to maintain minimum per-student funding levels, and could offer a greater match to states that commit to offering debt-free higher education for low- and moderate-income students. For additional detail on this proposal, see the Demos policy brief: The Affordable College Compact: A Federal-State Partnership to Increase State Investment and Return to Debt-Free Public Higher Education.

How Labor Markets Contribute to the Racial Wealth Gap

American households derive much of their economic security from the labor market, with earned income, employer-provided health coverage, paid leave, and workplace retirement plans offering greater opportunities to build wealth for the employees who have access. The greater a household’s income, for example, the more money household members have to save and invest. Meanwhile if an employer provides an affordable health insurance plan, employees often spend less than if they had to purchase their own coverage or risk incurring substantial medical expenses that can drain wealth. Pensions and 401(k)-type plans with an employer contribution offer a mechanism for employers to contribute directly to household wealth, adding to retirement savings. Yet labor markets are one of the primary drivers of the racial wealth gap, accounting for 20 percent of its growth in the last 25 years. In addition, unemployment, which causes many families to draw on and deplete their assets, explains an additional 9 percent of the growth in the racial wealth gap.

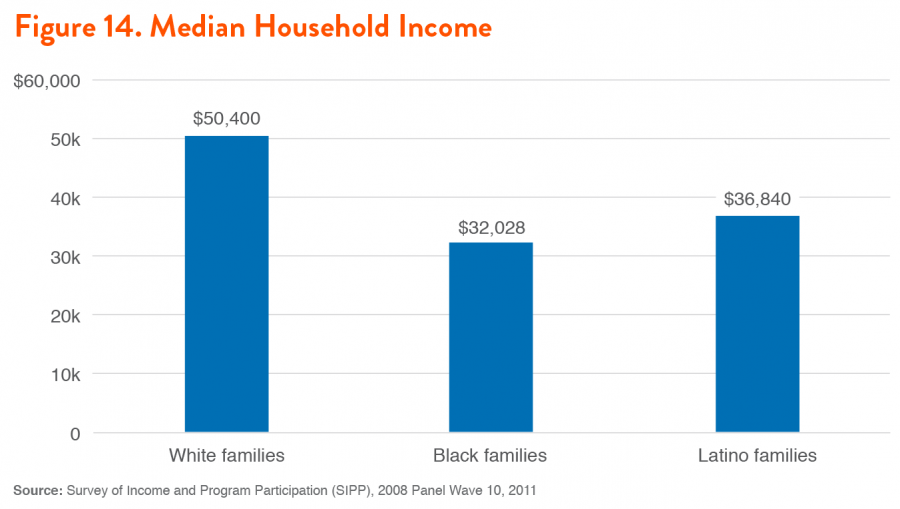

Disparities in labor market outcomes arise from a variety of sources, including employment discrimination, lack of geographic access to jobs, and disparate social capital. Income disparities affect both current consumption and wealth building opportunities. Median Black and Latino families have lower incomes than white families: while the typical white family makes $50,400 a year, the typical Latino family makes just $36,840 and the typical Black family has an annual income of only $32,028 (see Figure 14).

In addition to lower incomes, Black and Latino families also see less of a wealth return on the incomes they earn—in effect, they are less able to translate each additional dollar of income into wealth. For each dollar in income white families earn, they see a return of $19.51, compared to a return of only $4.80 on each dollar for Black families and just $3.63 for Latino families. A number of labor market dynamics contribute to these disparities: Blacks and Latinos are less likely to have jobs that include core employer-provided benefits such as health coverage, a retirement plan, or paid time off. As a result, families of color have fewer opportunities to save because they must use their current income to deal with more of life’s vicissitudes. Similarly, Black workers have higher rates of unemployment and longer average unemployment spells, which drains wealth and adds to labor market instability.

The following section will more closely consider the factors that contribute to disparities in labor market outcomes and assesses how equalizing family incomes and returns to income (the ability to translate a dollar of income into wealth) between whites, Blacks, and Latinos would impact the racial wealth gap.

Labor Market Policy Shapes the Wealth Gap

Racial and ethnic inequality in American labor markets was codified and maintained by law for much of U.S. history. It was not until the Civil Rights Act of 1964 that federal law prohibited job discrimination on the basis of race, color, religion, sex, and national origin. Yet public policy decisions—from the enduring exclusion of certain job categories to the protections of the Fair Labor Standards Act to immigration laws that inhibit workers from exercising their full rights in the workplace—continue to shape the U.S. labor market in ways that systematically disadvantage Blacks and Latinos, helping to explain why people of color bring in lower incomes and receive lower wealth returns than white families.

For most Americans, the vast majority of income comes from a paycheck. Black and Latino workers are not only paid less, but are also more likely to be employed in jobs that fail to offer key benefits such as health coverage, paid leave, or retirement plans. The disparity in benefits helps to explain why families of color accrue less of a return on each dollar of wealth earned than white families: Blacks and Latinos are more likely to pay for necessities like health care out-of-pocket and therefore, to have less to save and invest for the future. This also means that households of color are more likely to miss out on the tax incentives and wealth-building vehicles provided by employer benefits

Why don’t Black and Latino workers simply move into better-paying jobs? The lower rates of college degree completion discussed previously is one important factor. However, white workers with and without college degrees out-earn their Black and Latino counterparts with similar levels of education. The persistence of job discrimination is a critical part of the explanation for the lower incomes of Black and Latino workers. Here the problem is partly a failure of effective policy enforcement: employment discrimination on the basis of race or national origin has been illegal for decades, yet there is substantial research evidence that it endures, whether through overt bigotry or implicit bias. In addition, since Americans lead largely segregated lives, whites disproportionately benefit from social networking advantages. Because networks reproduce racial wealth inequalities, public policy interventions are required to disrupt this cycle.

For the Latino workforce in particular, immigration policy is a barrier to better jobs and higher incomes. While the nation’s worker protection laws officially extend to all employees regardless of immigration status, in practice immigrant workers face barriers to exercising their rights in the workplace, resulting in lower earnings. Limited English, lack of familiarity with the U.S. labor market, and concern about immigration status may also encourage immigrant workers to remain in occupations and industries they are familiar with, even if these jobs pay less and offer fewer benefits.

With the exception of those who are already very wealthy, Americans need good jobs to build assets. Yet, policy choices have contributed to the segregation of labor markets, both reducing the incomes of Black and Latino workers compared to whites and reducing the ability of people of color to turn additional income gains into wealth. As a result, labor market disparities are one of the primary contributors to the racial wealth gap. The next two sections highlight our empirical analysis exploring how the racial wealth gap would change if incomes and returns on income were more equal.

How Equalizing Incomes Affects the Wealth Gap

We tested the effects of eliminating income disparities among white, Black, and Latino families on the racial wealth gap by equalizing the patterns of household income distribution by race and ethnicity. In the current income distribution, white families are disproportionately likely to be at the top while Black and Latino families are overrepresented among lower income households . For our analysis, we estimated the income distribution of the white population alone and identified the thresholds for each income decile (for example, the top ten percent of white households in terms of income, the next ten percent after that, and so on); we then assigned weights to the Black and Latino households that appear in each decile of the white distribution until those households represent 10 percent of the Black and Latino populations. This test did not control for other characteristics that might distinguish those in any particular decile. In other words, we shifted the number of estimated households across the income distribution such that whites, Blacks, and Latinos were represented across the income distribution in equal proportions to their presence in the overall population.

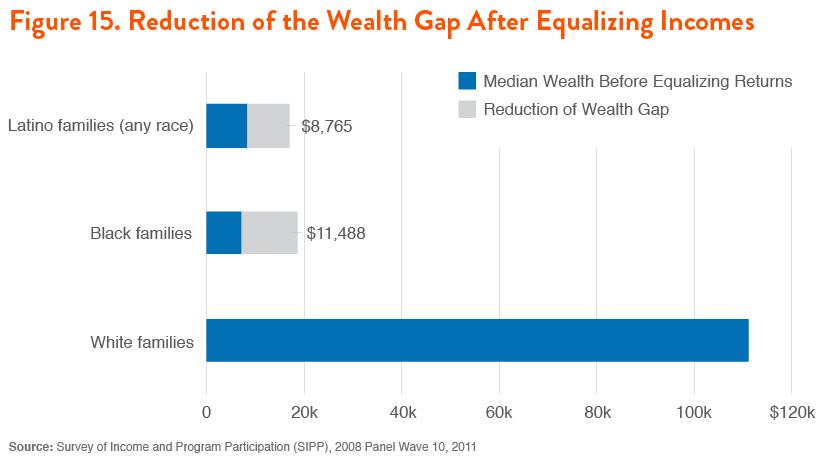

As a result of the redistribution, median wealth among Black households rises from $7,113 to $18,601—adding $11,488 to the median Black household’s wealth (see Figure 15). Median wealth among Latino households rises from $8,348 to $17,113—adding $8,765 to the median Latino household’s wealth. Those gains represent a 162 percent wealth gain for Black households, and a 105 percent wealth gain for Latino households.

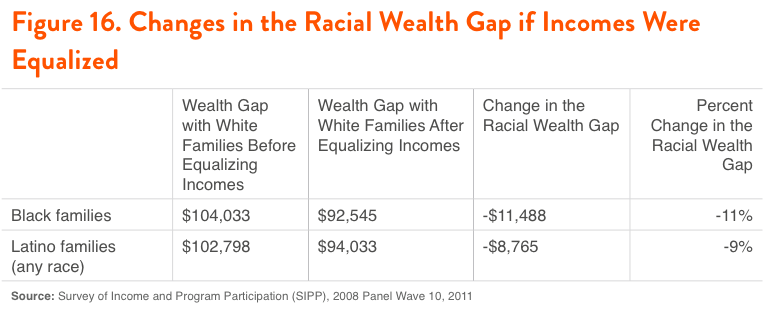

Equalizing Black and Latino incomes to match the white income distribution increases wealth among Black and Latino families who see higher incomes, while white wealth remains constant, modestly reducing the racial wealth gap. The wealth gap between white and Black families was decreases by $11,488, but leaves a remaining gap of $92,545. The change amounts to 11 percent of the racial wealth gap (see Figure 16). The wealth gap between white and Latino families decreases by $8,765, leaving a racial wealth gap of $94,033. The change in the racial wealth gap as a result of equalizing the income distribution is 9 percent.

How Equalizing the Return to Income Affects the Wealth Gap

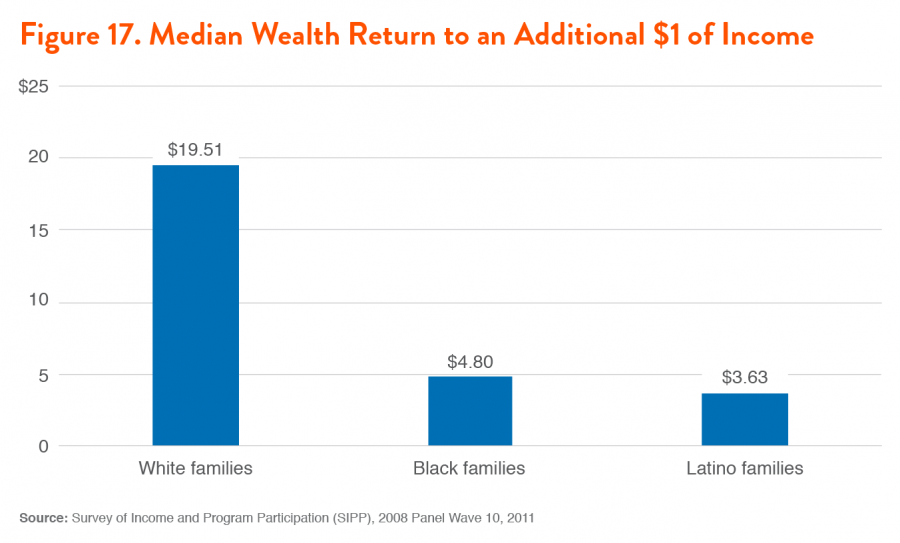

We also tested the effects of changing the return to an additional $1 of income for Black and Latino households to equal the return for white households. The first step in this model estimates the wealth returns to an additional $1 of income using a median regression model for the white population. That model estimates that white households experience a return of $19.51 in wealth on each additional dollar in income.

The wealth return to an additional dollar of income for Black households amount to $4.80—only 25 percent of the returns that accrue to white households. This means that for every dollar in wealth that accrues to Black families associated with higher incomes, a white family gets $4.06 (see Figure 17). Meanwhile, the wealth returns to an additional dollar of income for Latino households amount to $3.63—19 percent of the return for whites. This means that for every dollar in wealth that accrues to Latino families associated with higher incomes, a white family typically gets $5.37.

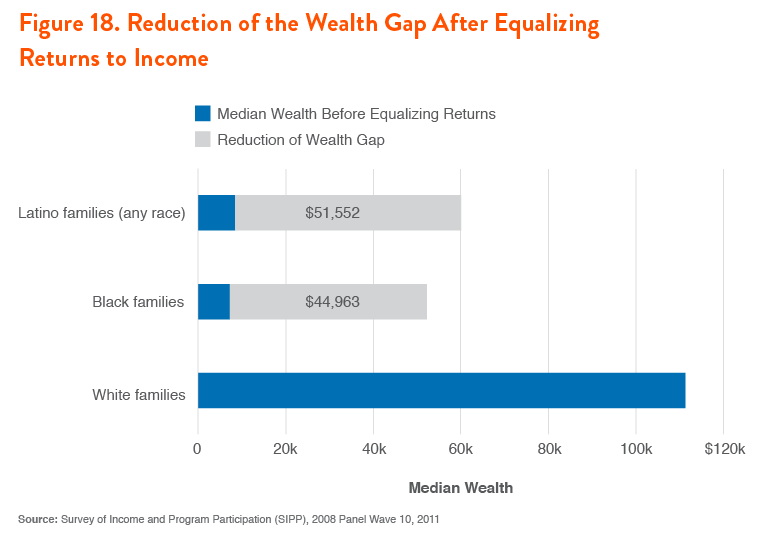

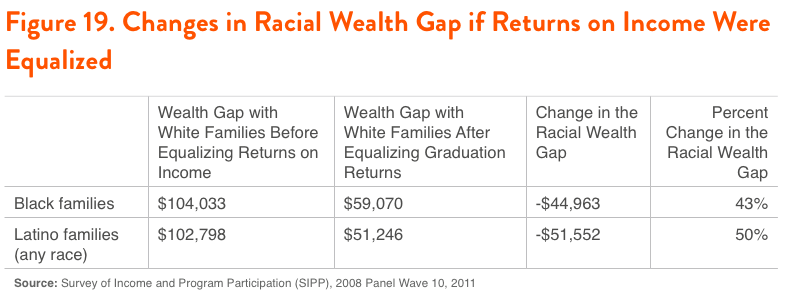

Improving Black families’ return to an additional dollar of income to equal whites’ returns increases Black families’ wealth by $44,963 to a total of $52,076—a 632 percent increase in Black household wealth. Meanwhile, equalizing Latino families’ returns to an additional dollar of income boosts Latino wealth by $51,552 to a total of $59,900—a 618 percent increase in Latino household wealth.

Equalizing returns to an additional dollar of income raises wealth among Black and Latino families while white wealth remains constant, substantially reducing the racial wealth gap. Equalizing the returns to income reduces the wealth gap between white and Black families by $44,963 to a total of $59,070 (see Figure 18). This is a 43 percent reduction in the Black-white wealth gap (see Figure 19). Meanwhile, the wealth gap between white and Latino families is reduced by $51,552 to a total of $51,246—a reduction of 50 percent.

Labor Market Policies to Reduce the Wealth Gap

The range of labor market policies that could boost job quality for Black and Latino workers—raising wages, improving benefits, and offering more opportunities for career advancement—is extensive, even before we consider measures to reduce unemployment and increase the ability to turn income into wealth. Below is a sample of three policies with the potential to shrink the racial wealth gap from income and labor market outcomes. The list is far from comprehensive.

- Establish a direct federal job creation program. Despite an improving economic outlook, Black unemployment remains high, and unemployment for Black teenagers is particularly widespread. A direct federal hiring program would put people back to work and employ workers to produce useful goods and services for the public’s benefit, such as maintaining and upgrading infrastructure, and providing child care, elder care, and cultural enrichment. By targeting communities where joblessness is much higher than the national average, this policy could significantly reduce unemployment among Blacks, while raising incomes and reducing the racial wealth gap in the process.

- Raise the minimum wage. Black and Latino workers are disproportionately likely to be employed in positions that pay the minimum wage or just above and would benefit the most from an increase in the federal minimum wage. With new research indicating that minimum wage increases have not reduced employment, a hike in the federal minimum wage from its current low rate of $7.25 would boost the incomes of many of the lowest paid Black and Latino workers and have the potential to decrease the racial wealth gap.

- Make it easier for workers to form unions. In earlier decades, white-dominated labor unions often acted to exclude Black and Latino workers from high-quality unionized jobs. Yet, today unionization rates are higher for Black workers than for white workers. Blacks and Latinos see greater wage premiums as a result of union membership than white workers and union membership does more to increase access to key employment benefits like health coverage and retirement plans for people of color than it does for whites. Making it easier for workers to form and join unions could therefore be expected to boost pay and benefits for Black and Latino workers and decrease the racial wealth gap.

Conclusion

When it comes to tackling the racial wealth gap, policies matter tremendously. Simply increasing rates of Black and Latino achievement (whether it is homeownership, college graduation, or income parity) is not sufficient to fully eliminate the gaps in wealth between Black and Latino families and their white counterparts. In almost every case, equalizing the returns to any given achievement makes a greater difference for the racial wealth gap than eliminating disparities in home purchases, college graduation rates, or wages. The challenge is that improving the economic returns that households gain requires confronting and changing the deeply entrenched structures discussed throughout this paper— from residential segregation to jobs that lack the benefits that enable households to build assets. Policymakers must act both to remove barriers to access and achievement and also challenge the deeply-rooted structures that reproduce disproportionate advantages for white households.

Our results suggest that policies that successfully address disparities in homeownership rates and returns to income are likely to be the most effective in reducing the racial wealth gap. At the same time, policy details matter. As policymakers craft proposals and evaluate legislation, the Racial Wealth Audit will be a valuable tool for understanding how policy impacts one of the most pressing questions of our time—the nation’s growing economic divergence along racial and ethnic lines.

Methodological Appendix

SIPP Data

The Racial Wealth Audit (RWA) analyses in this study utilize the Survey of Income and Program Participation (SIPP) 2008 Panel, Wave 10 from calendar year 2011. A nationally representative survey conducted by the Census Bureau, the SIPP includes rich information on survey participants’ household income, demographic characteristics, and participation into and out of government social programs, such as ‘Temporary Assistance for Needy Families’ (TANF). The SIPP is a panel survey following the same households for 2.5 to four years; the first panel was started in 1968. Each panel includes a large number of rotating waves with a diverse range of sub-topics. Wave 10 of the 2008 panel was chosen for our analyses because it includes the most recent comprehensive data on household assets.

Reweighting Calculations: Adjusting Factor Ratios Between Two Groups

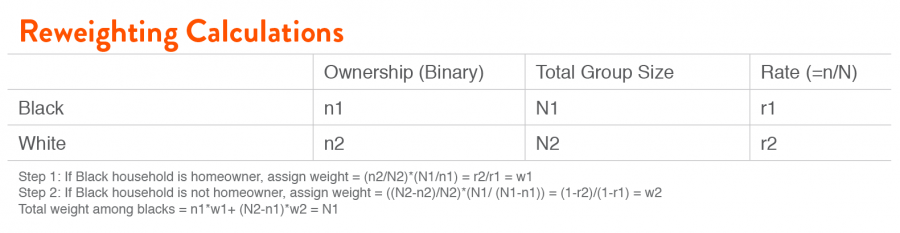

In order to model changes to the racial wealth gap under circumstances in which the rates of key wealth achievements are equalized by race and ethnicity, we shifted the distribution of households for each race/ethnicity subgroup using a reweighting technique in order to equalize the proportion households who have obtained a specific wealth asset, such as homeownership. In other words, in the case of homeownership, we increased the population weights of existing Black and Latino homeowners in the survey, such that they made up an equal portion of their respective subgroups as white homeowners make up among all whites. To present a simplified example, if the proportion of homeowners to renters among whites was 3/4, and 1/2 for Blacks, then this approach would reweight Blacks in the SIPP survey who own their homes from 1/2 to 3/4 of the entire Black sample population, and Black renters from 1/2 to 1/4 of the black sample population. Under this reweighted scenario, the ratio of Black homeowners to renters becomes equal to the existing current ratio of white homeowners to renters. This method keeps all other characteristics, including demographics within the Black homeowner population and Black renter population, respectively, constant. Since the reweighting technique does not apply any changes to the characteristics of the sample households in the survey, but rather shifts the proportions of particular households present in the population estimates, the method only changes the share of the sub-populations within the full population sample.

The following equations depict the mathematical calculations used to develop new weights to adjust the homeownership rates of blacks to white levels:

The technique outlined here to develop new weights to equalize rates of homeownership is applied to all three policy areas discussed in this report and for Blacks and Latinos. Because the SIPP household weights, which allow researchers to estimate all U.S. households, and our new weights are both probability weights, they can simply be multiplied to estimate the full U.S. population under the alternative scenarios we have envisioned in the three policy areas. For additional information on regression analysis with propensity scores, see ‘Weighting Regressions by Propensity Scores'.

Quantile Regression Estimates of Wealth Returns

For our estimates of differences in returns to homeownership, college education, and household income, we conducted quantile regression (QR) analysis at the 50th percentile, also known as median regression, to estimate typical wealth gains experienced by families who attain these achievements. Explanatory dummy variables within comprehensive multivariate median regression models captured predicted typical gains, or “returns,” resulting from the realization of these key wealth factors at the median. Models were conducted separately among whites, Blacks, and Latinos in order to estimate differential returns to these assets experienced by whites and households of color.

The key difference between quantile regression and Ordinary Least Square (OLS) regression is that the former calculates the outcomes of specific distribution percentiles, while the latter calculates estimates based on distribution means. QR is particularly important in the case of statistical predictions for distributions that are not normal, as it is the case with asset and wealth ownership. For example, an OLS regression model that calculates asset holding disparities between Blacks and whites will only predict averages (means) for both racial groups, thereby hiding important information about the within-group inequality. QR models solve this problem because they can be specified to different percentiles of the distribution, such as the median. In other words, they enable us to calculate predictions for wealth holdings among blacks and whites at every level of the distribution.

Until recently OLS has been the more dominant statistical approach because the calculations for quantile regressions were considered too tedious. However, strong increases in computing power over the last few decades make this argument less relevant today. Given that QR is a superior approach to explain relationships of variables that are highly skewed, as is the distribution of wealth in the United States, we used median regression, which allows us to predict the expected increase in wealth due to key factors at the median for white, Black and Latino households. While the regression models cannot provide causal associations, the returns to key factors represent an expected gain in wealth that is typically seen by households upon obtaining a particular asset.