Climate change poses a tremendous threat to Florida. Sea level rise, more intense precipitation, and stronger hurricanes increase the risk of natural disaster and imperil the state’s economy and its citizens’ safety. Compounding these dangers, increasing coastal population and development will put more people and property at danger. In years to come, those risks will lead to devastating damage if they are not mitigated. Florida has strong interests in limiting the extent of climate change and the state’s leaders should support efforts to enact strong national and international climate policies.

Florida’s climate is complex. It is influenced by the ENSO (El Nino-Southern Oscillation), the Atlantic Multi-Decadal Oscillation and other forces that sometimes act in concert, sometimes in opposition. This variability makes it difficult to isolate statistically the ongoing effects of climate change in the weather record and will continue to do so for decades to come. The consequence, however, is not to reduce or to defer the increasing threats but only to make them more difficult to understand, thus complicating efforts to build support for an adequate response. But, as this report shows, failure to act will be disastrous. A study by the Sandia National Laboratory found that Florida is one of the states most vulnerable to devastating climate impacts.

Climate Change and Increased Hurricane Intensity

The effects of climate change on hurricane frequencies and intensities have been the subject of much scientific investigation and inquiry. As they generate power from warm, moist air over warm ocean waters, hurricanes are becoming more intense as climate change continues to increase ocean temperatures. The current scientific understanding is that sustained warming will result in the more intense hurricanes becoming more frequent in Florida’s latitudes and the less intense hurricanes growing less frequent.

With climate change driven by increasing emissions, the frequency of the most intense Category 4 and 5 storms would be expected to increase by 80 percent by 2080, or by roughly one percent per year. Over the same period the frequency of the less intense Category 1-3 hurricanes will diminish by 38 percent. The implication is that hurricane risks are increasing dramatically because historically, Category 4 and 5 hurricanes have caused 86 and 48 percent of recorded hurricane damages, even though they represented only 24 and 6 percent of hurricane landfalls in the United States respectively. A study by Yale Economics Professor William Nordhaus, based on previous hurricanes that have struck the United States, found that higher winds cause more devastation, persist longer at damaging levels and generally affect a wider area.

Increased Risk of Economic Damage from Hurricanes

While hurricane risks are intensifying, Florida’s economy is changing in ways that put more people and property in harm’s way. The state’s population is growing and commercial and real estate development are again increasing in the coastal zone, despite the collapse of the real estate bubble. This trend is expected to continue. In fact, the potential loss from any given storm is expected to double in each decade. This prediction is consistent with Florida’s history over the period 1995-2010, a period spanning the real estate bubble, when the total loss exposure of insured property increased from $774 billion to $2.2 trillion, an annual increase of 7.5 percent per year.

Residential properties in the exposed areas are particularly vulnerable. Seventy-eight percent of houses, excluding mobile homes, were built before 1944 and 88 percent do not meet current building codes. For example, only six percent have hurricane shutters, or equivalent protection, and 54 percent connect roof to walls only by nails, toe-nailing, adhesives, friction or gravity. People are also vulnerable. Only one-third of vulnerable households evacuated in the face of Hurricane Andrew, despite evacuation warnings. In future category 4 and 5 storms, more than a million households might have to be evacuated from exposed areas in South Florida, a process that could take 24 to 48 hours.

The Florida Office of Insurance Regulation, which oversees the Florida Hurricane Catastrophe Fund and private insurers, estimates that in 2010 the insured losses of a storm with a 50-year return period would be approximately $40 billion. Total economic damages are estimated by multiplying insured losses by two. However, this rule-of-thumb is a gross underestimate. Not all storm hazards are covered by conventional property insurance – flood damages, for instance. Also excluded are the potential deaths and injuries from a severe hurricane. The losses to businesses that are closed because facilities or infrastructure are damaged or potential customers are displaced are not accounted for.

The loss from closed businesses is particularly important in Florida because tourism is one of the state’s most important industries. 85.9 million tourists visited Florida in 2011 almost all from out-of-state. In 2010, direct tourist spending exceeded $62.7 billion per year and generated $3.8 billion of state sales tax revenue, not including the significant impacts of indirect expenditures resultant from tourism. Over one million people are directly employed in the tourism industry and that number increases significantly when indirect employment is taken into account, largely in lodging, restaurants, and retail stores. Natural disasters have immediate and long-lasting effects on tourism. After Florida was struck by several hurricanes in 2004, causing disruptions and evacuations, surveys of potential tourists found that 20 percent would not return next year. Severe hurricanes with higher frequencies could potentially cripple the tourism industry, with major impacts on associated industries that make up more than a third of Florida’s economy.

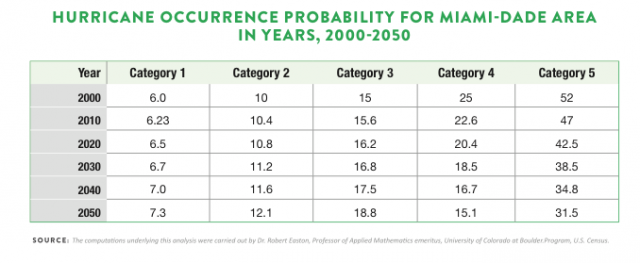

When these projections of higher sea levels, more frequent intense hurricanes, and increased property values at risk are brought together in an integrated analysis, using numbers that represent the best current estimates of Florida’s scientists, the results are ominous. The following table shows the changing return periods of Category 1 through 5 hurricanes from 2000 through 2050 striking the Miami-Dade region. Though the probabilities of moderate hurricanes decline, the probabilities of major hurricane strikes increase by 50 percent over the period. By 2050 there would be about a one in ten chance that a Category 4 or Category 5 hurricane would strike the Miami-Dade area in any year. Other areas along Florida’s coast face similar changes in risks. Since the higher intensity storms create by far the greater damage, overall risks from hurricanes increases significantly.

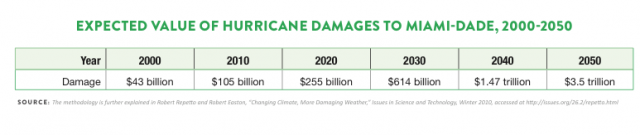

In order to construct an overall risk analysis, these return periods, expressed as probabilities, were combined with the damage function estimated by Nordhaus and an estimate by MIT professor Kerry Emanuel that a hurricane with 130 miles per hour winds striking Miami in 2000 would result in damages of $87 billion. Damage estimates also factored in the effects of rising sea levels and the increase in coastal population and value at risk.

Within the table below, expected losses are the damages that would be suffered from a storm of each intensity, multiplied by the probability of such a storm occurring, and then added up for all possible storms. Expected losses represent the actuarially fair value of hurricane damages to the region—the amount that insurers would have to collect in premiums (without overhead) to break even over time. Expected losses rise dramatically, more than doubling in each decade because of the combined effects of climate change on hurricane intensities and sea level, along with the increase in value at risk. Private insurers would have to raise rates dramatically or withdraw from the market and the state’s Citizen’s Property Insurance Corporation will need much greater taxpayer support. At this time, unfortunately, the Florida Hurricane Public Loss Projection Model, developed for the Office of Insurance Regulation, does not yet incorporate the effects of climate change on hurricane frequencies because of the problems of separating these effects from shorter—term variability.

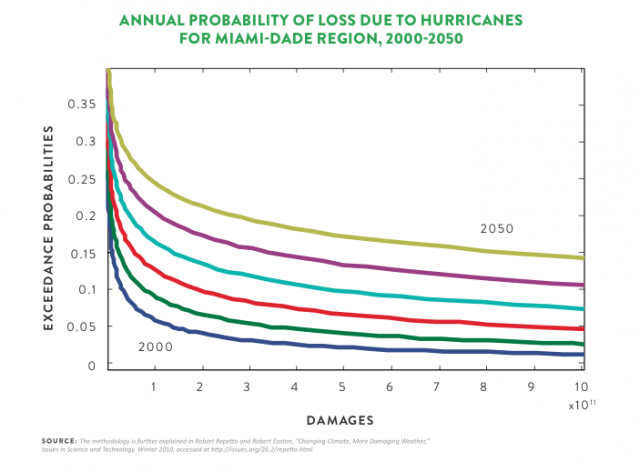

Another depiction of increasing economic risks comes through loss exceedance curves, which are widely used in the insurance and other financial industries to measure risk exposure. A loss exceedance curve is the probability that a loss will be incurred that is equal to or greater than some amount. Loss exceedance curves for each decade for the Miami-Dade area are plotted in the following graph.Two things are immediately evident. First, the curves “flatten out”as loss amounts rise.Though probabilities of occurrence decline as maximum wind speeds rise, this is offset by the exponential increase in damages, so the probabilities of loss – combining the two – hardly falls. By 2030 there will be a 1 in 12 chance of a loss exceeding a trillion dollars. Second, the loss exceedances rise rapidly over time. For example, the probability of damages exceeding $200 billion rises from about 1 in 25 in the year 2000 to more than 1 in 5 by the year 2050. The likelihood of even much greater losses rises almost as rapidly.

Comparable analyses would likely reach similar conclusions for urban areas all around Florida’s coastline, from Pensacola in the Gulf to Jacksonville in the Northeast. The implication of Florida’s own best estimates, when put together, is that climate change is sharply increasing the risks to its economy and citizens and substantially increasing the likelihood of catastrophic damage.

Impact of Sea Level Rises and Higher Storm Surges

One of the clearest impacts of climate change is the documented rise in sea levels, which has been taking place along Florida’s coasts at more than two centimeters per decade. Higher atmospheric temperatures heat the oceans and water expands as it warms. Sea levels rise further as melt waters from glaciers and continental ice sheets pour into the oceans at high latitudes. This process is expected to accelerate. Sea levels are projected to be three to seven inches higher by 2030 (over 2010), nine to 24 inches higher by 2060, and 39 inches higher by 2100, and the rise will continue long thereafter.

Even apart from larger storm surges, these sea level rises will have major impacts on coastal Florida, where 80 percent of the state’s population lives. Because so much of the shoreline is flat and low-lying, the impacts of even small rises extend far inland. Taking tidal variations into account, a one-foot rise can move the shoreline inward by more than a thousand feet. Most of this inundation will affect undeveloped land, especially in South Florida, replacing upland plant communities with mangroves and marshes and replacing those with tidal flats and open water. Commercial and recreational fisheries dependent on those coastal ecosystems and estuaries for spawning will be damaged along with many bird and animal populations.

Faster onshore winds from more intense hurricanes will push more water inland, generally creating higher storm surges. Sea level rise and the consequent landward movement of the shoreline will increase the damages from storm surges that occur when violent storms approach land. Florida is extraordinarily vulnerable to storm surges because of its location, its topography and the concentration of population and development along the coast. A recent FEMA study estimated that within the impact area of the historical hundred-year coastal storm surge, there were more than 3.9 million people in the year 2000, almost 25 percent of the state’s population. Florida has considerably more people at hazard than any other state and what had been known as the hundred-year flood is becoming more frequent. Nearly the entire coastline is at risk.

As storm surges increase and move inland, damage risks will escalate. For instance, 2005’s Hurricane Wilma resulted in a seven-foot high surge in Dade County and, according to a FEMA study, now has a 76-year return period. When sea levels have risen one foot, the return period for the same seven-foot storm surge would be only 21 years. When the sea has risen 2.13 ft, the return period for the same seven-foot storm surge would be five years. A storm surge similar to Hurricane Wilma will happen with about 15 times the frequency experienced in the past, just because of sea level rise. Moreover, the storm surge associated with Wilma, increased by a two foot sea level rise, would have caused at least 30 percent greater damages in Dade County than it actually did.

NOAA’s National Hurricane Center has carried out extensive modeling for specific regions to determine the probable effects of hurricanes on the height of storm surges. Based on this model’s results, the Florida Division of Emergency Management has created an atlas of potential storm surges around Florida’s coastlines. The amount of land affected by surges would increase substantially for more intense hurricanes, threatening extensive areas of urban development. The following table, based on NOAA’s SLOSH model, illustrates the impact of hurricane intensity on the height of maximum storm surge. Rising sea levels and more frequent intense hurricanes combine to raise the risks of storm surges and flooding dramatically.

For a one-foot increase in sea level, property losses will amount to many billions of dollars, more than $4 billion in Southeast Florida alone. A study focused just on the Florida Keys found that a two-foot rise would inundate 70 percent of the land area, flood out 17 percent of the population and 12 percent of the property value. This study, based on detailed topographic analysis, also found that the damages rise disproportionately as topographical barriers are toppled over.

Sea level rise will also greatly exacerbate existing problems of both water supply and drainage. South Florida’s complex public water management system is already under pressure from rising demand and limited capacity. Climate change is expected to reduce rainfall in southern Florida, increasing vulnerability to droughts like those of 2006-2010. Cities and towns in the region draw water from underground freshwater aquifers. Saltwater intrusion into these aquifers because of sea level rise and excessive pumping already threatens the public water supply in the densely populated region from the Florida Keys to Palm Beach.

Supplies in Florida’s two most populous counties — Miami-Dade and Broward— will be diminished further as the salt water boundary pushes inward from the Atlantic and infiltrates the Biscayne aquifer.Those areas may be forced to restrict withdrawals for irrigation and replace previous supplies by building expensive desalinization plants. Simultaneously, sea level rise will reduce the capacity of storm water drainage systems that carry excess water to the sea during periods of potential flooding by as much as two-thirds by 2040, increasing the risks of flooding from more intense rainfall events.

Long-Term Economic Impact of Climate Change

The long-term economic impacts of climate change will be most severe on Florida’s attractiveness as a destination for retirees and seasonal migrants. Second homes for those who winter in Florida constitute roughly eight percent of the state’s housing stock. For decades Florida has also been the favorite destination for retirees who move out of their home states, but that lead is shrinking: Florida was the destination for 26 percent of inter-state retirees in 1980 but only 16 percent in 2008. Still, retirees bring at least $2.2 billion in outside annual income to the state from pensions, social security and other retirement income.

A favorable climate, attractive waterfronts, and affordable housing have been the main draws, but increasing storm surges and hurricanes and rising insurance costs would change all that. Florida’s population is aging: the largest population increase in the coming decade will be people over 65. They are risk-averse. Economic studies estimate that such households would be willing to pay as much as nine percent of their income to reduce the likelihood of a natural disaster with a 50-year return period (currently a Category 5 hurricane) by half. This indicates how unwilling those relocating will be to live in locations where such catastrophic risks are not decreasing but are increasing rapidly.

Impact of Climate Change on Florida's Natural Environment

Risk to the Everglades

At the greatest risk of damage from climate change is the Everglades watershed, which would be extensively inundated by saltwater in its southern reaches by mid-century. The economic losses from tourism alone would amount to nearly a billion dollars in direct expenditures (at 2007 levels) and an equal amount in indirect expenditures. Also lost would be some of the important ecosystem services that the Everglades now provides, such as recharge of freshwater aquifers, improvement of water quality through filtration and sediment deposition, flood protection, and habitat for many species of plants and animals.

Beach Erosion

Florida currently spends $200 million per year in public funds in beach protection and restoration, recognizing that its beaches are an invaluable tourism and recreational asset. Yet, Florida’s beaches are in danger as beach erosion and the breaching of barrier islands along Florida’s coasts accelerate due to rising sea levels and storm surges. Eroding beaches destroy thousands of homes in the United States every year and reduce the value of surviving beachfront property. In 2002 more than half the beaches in Florida were eroded and, of these, three-quarters were critically eroded and less than half of those were being managed.

A 2005 assessment found that beaches drew nearly 40 percent of tourists to Florida, more than 90 percent of those coming from out-of-state. Direct spending by beach tourists contributed 3.9 percent of Florida’s GDP and created half a million jobs. Indirect expenditures doubled those amounts.

Ocean Acidification and Loss of Marine Biodiversity

Climate change will have other significant impacts on Florida’s economy. Rising ocean temperatures and acidification will harm the marine environment as the seas absorb heat and carbon dioxide from the atmosphere. Warmer water combined with greater fertilization by mineral-laden dust blown across the Atlantic, will exacerbate the “red tide” and other algal blooms that close beaches and kill marine life by the millions. Vibrio- related illnesses from eating contaminated shellfish, which have doubled in incidence in the last decade, will continue to increase.

Acidification and higher water temperatures will kill off Florida’s corals, a major tourist attraction in the Keys and important fish habitat. Acidification also affects plankton and other organisms at the base of the fisheries food chain as well as such important marine resources as shrimp, lobster and other crustaceans. Tourism and recreational fishing, both important to Florida’s economy, will be harmed. Non-residents made 20 million fishing trips in Florida’s waters in 2011, the second highest total in the country.

The Way Forward

Florida’s own scientific estimates indicate that the state’s economy and people face rapidly rising risks of catastrophic damages. Florida’s leaders, whether in politics and government or in the private sector, have compelling reasons to support strong, immediate policies at the state, national and international level to reduce greenhouse gas emissions and to mitigate the growing risks of global warming. Florida’s people, who ultimately bear those risks and will suffer the damages, should compel their leaders to do so.

Download PDF for Endnote Sources