Introduction

The rapid and unrelenting rise in student debt over the past decade has put college affordability and student loan policy at the forefront of the national political conversation. By now, the numbers are familiar: 7 in 10 bachelor’s degree recipients must borrow if they hope to get a degree, and average debt at graduation has now exceeded $30,000. Due to expanded undergraduate and graduate enrollment, stagnant wages, and higher tuition spurred in large part by state disinvestment, the amount of student debt in the U.S. economy has increased by nearly a trillion dollars in the past decade alone.

If nearly 70 percent of graduates are borrowing, 30 percent (including 35 percent of public college graduates) are not. Who are these students?

Unlike two decades ago, when fewer than half of students borrowed for a four-year degree, it’s difficult to find students today who can graduate without debt, even at public colleges and universities. Indeed, it’s increasingly difficult to find those who can receive an associate degree without taking on loans. Borrowing is essentially a requirement for black and low-income students. And high costs and the universality of borrowing has led to a system in which many students are taking on debt without graduating, which massively increases the risk of struggling to repay or defaulting on a loan. Both average borrowing and the risk associated with dropping out with debt are inequitably distributed by race and class. These worrying trends have led policymakers and advocates to focus on the need for the U.S. to return to a system of affordable—including tuition-free or debt-free—public college, in which students could finance a two- or four-year degree simply through part-time work or exceedingly modest family savings.

As policymakers begin to develop comprehensive proposals, it’s important to understand which students are currently able to graduate without debt. If nearly 70 percent of graduates are borrowing, 30 percent (including 35 percent of public college graduates) are not. Who are these students? What type of family or financial resources do they have at their disposal? What are their work habits? In short, what does it take to graduate debt-free these days? This brief will answer these questions, allowing for a deeper understanding of what levers, policies and practices will be necessary to ensure all students can attend a state college or university without taking on debt.

Methodology

All calculations are from the U.S. Department of Education National Postsecondary Student Aid Survey 2012 (NPSAS:12). All figures are for bachelor’s degree recipients from public institutions. Due to sample size issues, some data on Asian Americans and Native Americans are unavailable. Results for independent students and dependent students are noted separately where available and appropriate.

The Demographics of Debt-Free

The need to borrow for a four-year degree differs substantially by race and income. In fact, at public institutions, 81 percent of black students must borrow for a bachelor’s degree compared to 63 percent of white students. Low-income students—those who receive Pell Grants—are overwhelmingly more likely to borrow for a degree as well: 84 percent of Pell recipients who graduate must borrow compared to less than half (46 percent) of non-Pell recipients.

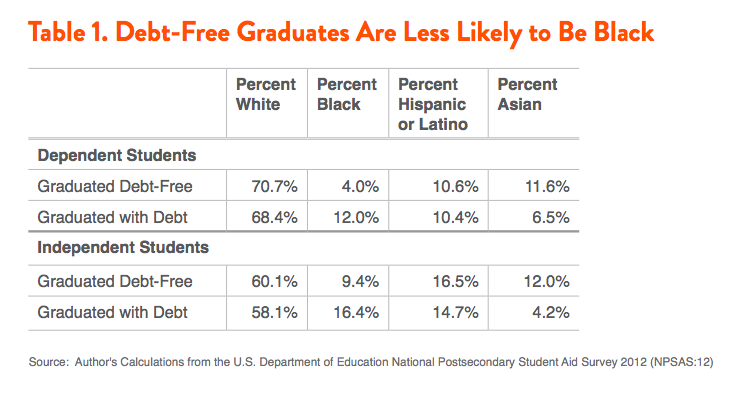

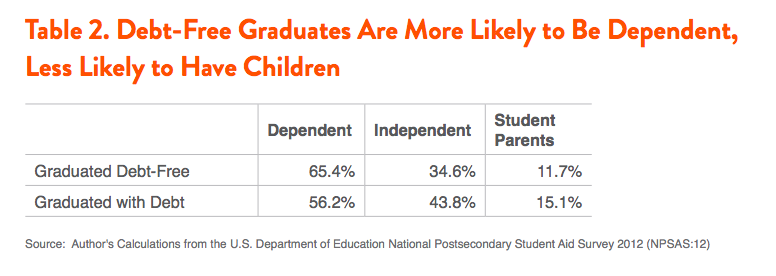

It’s perhaps unsurprising, then, that black and low-income students make up a greater portion of indebted graduates among both dependent and independent students. In fact, among dependent students, just 4 percent of debt-free graduates are black, compared to 12 percent of indebted graduates. Asian students make up nearly 12 percent of debt-free graduates. Debt-free graduates are also more likely to be dependent students, which makes sense given that independent students by definition do not receive direct financial support from parents in paying for college. Indebted graduates are also more likely to be student parents themselves – more than 1 in 7 indebted graduates have dependents of their own.

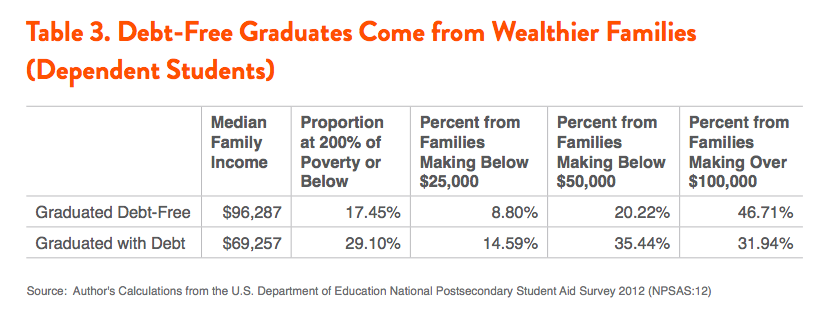

Naturally, much of this overlaps with family income. Almost half of debt-free graduates (46.7 percent) come from families making more than $100,000 annually, and median family incomes for those who graduate without debt are over $27,000 higher than for those who must borrow. Students who borrow for a bachelor’s at public colleges are much more likely to come from families making around or below $50,000—approximately the median U.S. household income—and far more likely to come from families at 200 percent of the poverty level or below.

In some ways, this phenomenon may even be understated. For example, the unrelenting rise in college cost may not only result in the need for some students to borrow more, it may be constraining opportunity and preventing students from attending four-year colleges, or making them avoid college altogether. Additionally, research suggests that while small amounts of student debt may be positively associated with graduation, amounts above $10,000 are negatively associated with the ability to complete a degree. Thus, the students who borrow and make it through a four-year degree program only represent a subset of those affected by the move to a system that requires greater levels of borrowing.

Federal Benefits Are Not Generous Enough to Prevent Borrowing

The U.S. has a system of supports to help low-income households defray college costs. The most obvious example is need-based financial aid, from the federal Pell Grant to state-based grant and scholarship programs, which attempt to lower the cost of attendance for low-income households. The aim of need-based aid is twofold: to ensure that cost is not a barrier to attending and completing college, that college costs are not more of a burden on low-income communities than on their high-income counterparts. Similarly, the federal government has a series of means-tested benefit programs like the Supplemental Nutrition Assistance Program (SNAP), the Special Supplemental Nutrition Program for Women, Infants, and Children (WIC), Temporary Assistance for Needy Families (TANF), and Supplemental Security Income. Many of these programs are run through state or local agencies, but the purpose is generally to provide both financial and food security such that recipients can participate in the broader economy and meet basic needs.

However, despite their initial promise, neither the Pell Grant nor federal means-tested benefits are generous enough to prevent students from borrowing for a degree. Given that indebted graduates come from less-wealthy households, it is to be expected that college costs make up a greater portion of their family income. But even factoring in grant aid, for both dependent and independent students, the net price of college—what is left to be paid after grant and scholarship aid—takes up 12 percent more of household income than it does for debt-free graduates.

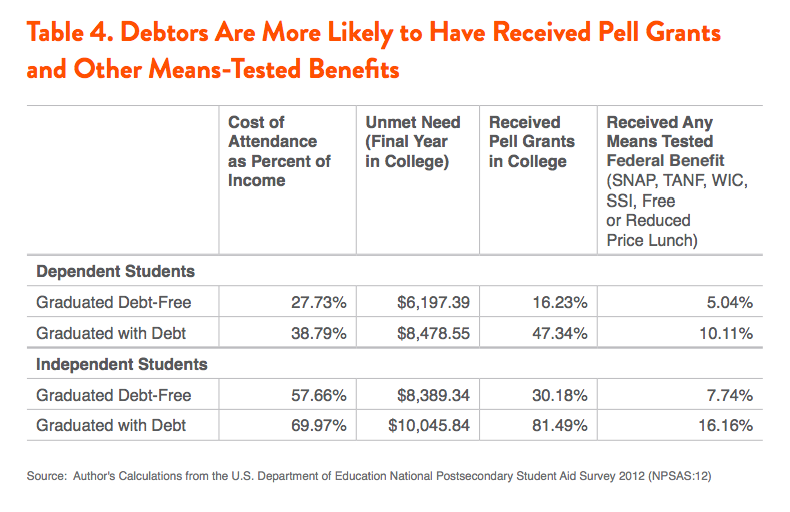

Those who graduate with debt have thousands of dollars more in unmet need (the cost of attendance minus grant aid and expected family contribution) for college— despite the fact that they are more likely to report having received Pell Grants and other means-tested benefits. In fact, among dependent students, over 47 percent of indebted graduates also received Pell Grants, compared to just 16 percent of debt-free graduates. For independent students, the difference is far starker: 81 percent of independent indebted graduates received Pell Grants, compared to 30 percent of independent students who graduated debt-free. Even after receiving an additional voucher, worth up to $5,500, Pell Grant recipients still had substantial unmet need during their time in school. In short, families who do not qualify for Pell Grants are at such a substantial financial advantage that they are still far more likely to graduate debt-free.

In theory, some student borrowers could be eligible for federal tax benefits, such as the American Opportunity Tax Credit (AOTC) or the tuition tax deduction, which lower the tax liability of those who have paid tuition and fees over the previous tax year. These benefits have been widely criticized for their timing—benefits do not come until well after tuition bills have already been paid—but it is unlikely that many borrowers are even benefitting from them in the first place. A recent New America study found that a full 40 percent of undergraduate students are ineligible for any tuition tax break—most notably the AOTC. This is primarily due to the fact that costs such as room and board, transportation, insurance, child care, and medical or family expenses are not included in eligible costs. Thus, students who may receive a Pell Grant that covers a large portion of tuition and fees, but leaves substantial unmet need for other costs, would not receive much, if any, benefit from the tax credits.

In addition, the AOTC in particular is only partially refundable, meaning low-income households with no tax liability receive only a fraction of the credit that middle- and upper-middle class households receive. In short, it’s exceedingly unlikely that student borrowers are receiving a later tax advantage that helps them make up ground vis a vis those who do not have to borrow. If anything, the opposite is likely true: higher income non-borrowers also have the chance to deduct tuition or take advantage of tax benefits that put them on more solid financial ground.

Debt-Free Graduates Get More Help from Families

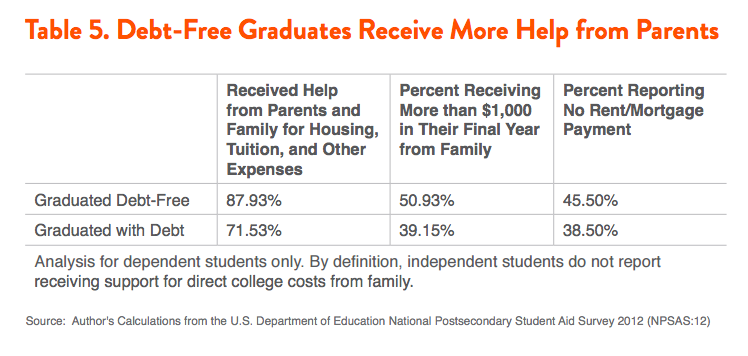

We know that debt-free graduates come from families with higher incomes. This leads to higher levels of support from family in paying for direct college costs, including tuition and living expenses. Nearly all (88 percent) of dependent debt-free graduates report receiving help from family for housing, tuition, and other expenses. Over half of debt-free graduates report receiving more than $1,000 from their parents in their senior year alone—a number that could very well underestimate the amount of support received, given that students may not report tuition as family support, since it is paid directly to the college without passing through the student’s hands. Debt-free graduates are also more likely to report that they paid no rent or mortgage payment in their senior year. This is particularly important, given that housing or room & board make up substantial portion of a student’s cost of attendance, and thus a substantial piece of the borrowing puzzle. Some students receive enough help from family or other sources to cover the totality of these costs, placing them further ahead of students who have to contend with net tuition, living costs, and other necessities.

Credit Card Debt Isn’t Replacing Student Debt, It’s Adding to It

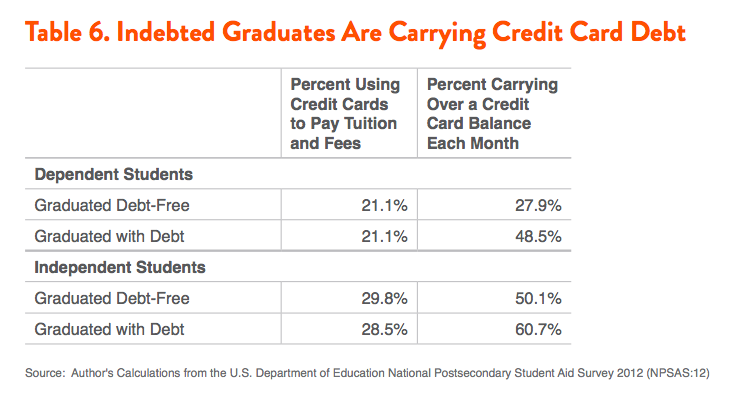

One theory for how students can graduate debt-free is simply that they’re using another mechanism to pay for college—namely credit card debt. By putting tuition and fees on a credit card, which some institutions allow, some students could be bypassing student loans but still be in relatively similar financial situations. In fact, were this the case, we would actually want more student borrowing, given the lower relative interest rates on student loans vs. credit cards.

Unfortunately, this theory does not show up in the data. Debt-free graduates and indebted graduates both use credit cards to pay tuition and fees at virtually the same rates, among both dependent and independent students. And student debtors are far more likely to carry over a credit card balance each month, indicating that they face other debt burdens as well, many of which can come with even higher interest rates than student loans. Demos has previously reported that contrary to popular imagination, credit card debt is often taken on in service of necessities and medical payments, rather than not living “within one’s means.” This seems to extend to college students as well—those who need to borrow to pay for college costs are also unable to pay off their consumer debt each month.

Debt-Free Graduates Are Less Likely to Work Long Hours, Multiple Jobs

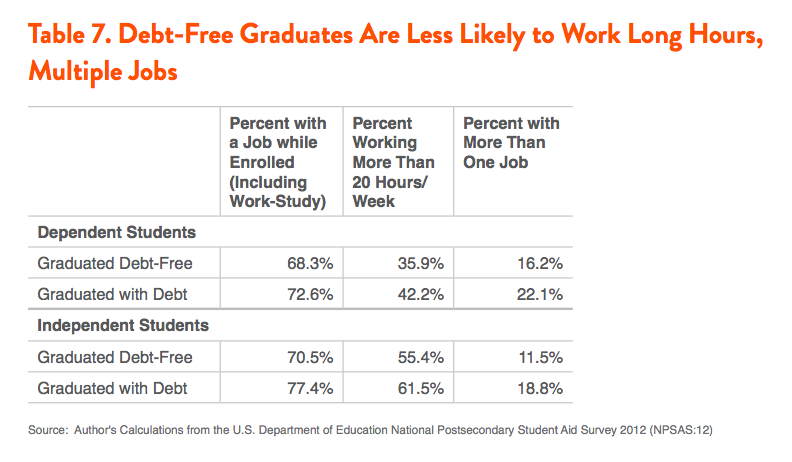

Most college graduates report having worked during college. And indeed, research suggests that some work is positively associated with graduating. But too much work, roughly 20 or more hours a week, is negatively associated with graduating, and presents a burden on students that prevents them from fully focusing on academics, relevant internships and networking, or other avenues that might help find a job or career after graduation.

Another theory about student debtors is that they simply are borrowng instead of working, and could achieve a degree with less debt by working part-time or full-time. This theory is not borne out in our comparison. While most graduates work, borrowers are actually more likely to work multiple jobs or work more than 20 hours a week. This is likely due to the fact that the net cost of college has far exceeded both minimum and median wages, rendering it nearly impossible to pay for college through work alone. In short, it is simply not the case that student borrowers are substituting employment for debt—they are working at higher rates in addition to taking on loans.

This puts to rest any notion that today’s students display a sense of entitlement or short-termism, borrowing rather than “working their way through school.” The fact is, while contending with less generous public subsidies and financial aid relative to college costs, students cannot rely on employment alone to pay for college costs. Most students work while in college, but some students seem to supplement their employment with substantial family resources, allowing them to graduate without borrowing.

Attending Community College Does Not Mean a Debt-Free Bachelor’s

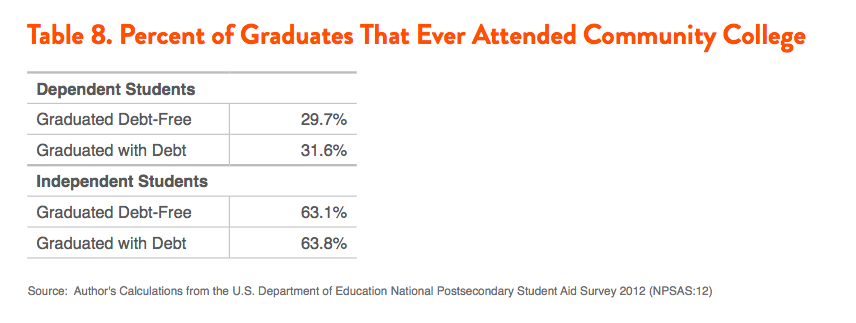

Another debt-free pathway to a bachelor’s degree could plausibly run through community college. Many state systems—most notably California—encourage students to attend low-cost community college before transferring to a public four-year institution in order to receive a bachelor’s degree. And it certainly stands to reason that attending an institution with relatively low tuition for two years would save many students the need to borrow much, if at all, for college. Yet this does not seem to be the case.Among both dependent and independent students, bachelor’s recipients who borrow for college report having attended a community college at virtually the same rates as debt-free graduates.

In addition, a 2012 study by the loan guarantor TG found that community college transfer students borrow nearly the same amounts as those who start college at four-year institutions. One possible explanation is that despite the relatively low tuition of community college (at least relative to public four-year institutions), students must also pay for living expenses, transportation, books & computers, food, child care and other necessities, making the total cost of attendance between community college and four-year institutions closer than they may appear. Another is a “bait and switch” of financial aid: there is evidence that many colleges also provide substantial grant aid to prospective freshmen in order to up the odds of attendance, and reduce financial aid packages in later years. If so, community college transfer students may be offered substandard grant aid packages, given that they are often transferring as sophomores, juniors, or seniors. Finally, community college students may not experience seamless credit transfer policies, forcing them to attend (and thus pay for) college longer than students who start and finish at a single institution. Regardless, due to low wages, a lack of credit transfer, or insufficient grant aid, attending community college does not seem to appreciably diminish the need to borrow for an undergraduate degree.

Conclusion and Policy Recommendations

The minority of students fortunate enough to graduate from public colleges without debt are doing so due to some built-in privileges. These are students who come from greater means, have higher support from parents, and do not need to work long hours or take on credit card debt in order to make ends meet while in school. They have lower unmet need, despite being less likely to receive Pell Grants and other benefits. College costs are simply a smaller burden for them.

A return to debt-free college is imperative, not just because it would boost access and attainment, but because our current system is inequitable. Fortunately, there are mechanisms to make it so that African American students are not overrepresented in our student borrower population, and working-class students do not face a greater burden of college costs than those from high-income families. Possible solutions include:

- Expand eligibility for Pell Grants and substantially increase the award to align with the cost of attendance. The federal Pell Grant, when originally conceived, covered nearly three-quarters of the total cost of attending college. But due to decades of political neglect, the maximum Pell Grant today covers less than one-third of college costs. If the U.S. indexed the federal Pell Grant to cover a set amount of college costs, recipients could be sure that their grant aid would mean something, and actually reduce unmet need no matter where they attend.

- Expand funding to Public Historically Black Colleges and Minority Serving Institutions. As state policymakers have systematically reduced per-student higher education funding over a period of decades, public Historically Black Colleges and Universities (HBCUs), and other Minority Serving Institutions (MSIs) are often last-at-the-table for funding from a dwindling state pie. In fact, institutions in Maryland and South Carolina have recently sued states for inequitable funding compared to public flagship and other state colleges. States have been derelict in providing funding for land-grant HBCUs, while federal funding through Title III of the Higher Education Act has done little to help these institutions keep up with predominately white colleges. These institutions are tasked with educating large numbers of our country’s black students—who again, are overrepresented in the borrower population—while contending with the legacy of institutional racism and the racial wealth gap it created. Given these realities, Congress should expand the scope and funding for HBCUs and do so in a way that translates to lower net prices and unmet need among black students.

- Guarantee that students who receive means-tested benefits receive enough aid to cover all college costs. Currently, students who receive means-tested federal benefits and come from low-income households are eligible for an “auto-zero” Expected Family Contribution distinction on the Free Application for Federal Student Aid (FAFSA). In theory, this means that the federal government is explicitly acknowledging to these students that they do not have any additional means to pay for college costs. But in practice, this distinction does not guarantee that their full need is met, or that they will receive grant aid sufficient to cover all, or even most, college costs. Rather than having a meaningless distinction, the federal government could require that by some combination of federal financial aid, state and institutional grants, the lowest-income students will have no unmet need at public two- and four-year institutions.

- Expand Federal Work Study benefits and eligibility. Federal Work Study (FWS) is a very popular, but very small federal program—appropriated at less than $1 billion last year. Additionally, like other campus-based aid programs including the Perkins Loan Program and Supplemental Education Opportunity Grant (SEOG), the formula for allocating work study leaves out students at many public institutions, including community colleges and regional public four-year colleges. We know that student borrowers are more likely to work, and work longer hours, than debt-free graduates. So by expanding Federal Work Study and making it a regular part of students’ financial aid packages, working-class students would see a wage boost, both reducing the likelihood that they will work long hours and reducing the need to borrow for college.

- Create a federal-state partnership to encourage state investment in higher education. While expansions in student aid and other benefits can help level the playing field for students, the decline in purchasing power of federal financial aid is a direct result of a decades-long decline in per-student state support for higher education. It is in the interest of the federal government to reinvigorate state investment, which could be done through a new federal-state partnership that rewards states for creating a guarantee of affordability for working- and middle-class students attending public 2- and 4-year institutions.